What is the cash reserve ratio?

In today’s world, the economy plays a vital role in the progress of any nation. We are living in a globalized world, where one nation has become dependent on another. None is able to meet the daily requirements of its people independently. In the era of advanced and dynamic technology where the whole world has become a single market, it is very difficult for a nation to survive only on the basis of indigenous product, capacity, or skill.

We are in the age of Liberalisation, Privatisation, and Globalisation i.e. LPG, in which the management of the economy of a country becomes complex. This complexity leads to demands of setting up various highly professional organizations at the international level as the likes of the World Bank, International Monetary Funds, etc. This phenomenon gave birth to the central bank which is a supreme regulatory body in a nation. Hence, these organizations make several rules and regulations to regulate the economy.

Read Also: Impact of Panama Papers on Indian Market

Central Bank makes various type of policy to regulate the economy of the nations. ‘Reserve Bank of India’ is the central bank of India which makes monetary policy and fiscal policy of the nation.

Cash Reserve Ratio i.e CRR is a tool of the central bank for the purpose of monetary control. In other words, a Monetary policy requires many tools and CRR is one of them.

Monetary Policy

Monetary policy is a powerful instrument for improving the macroeconomic position of a country. It is an important aspect of economic policy. Hence, the objectives of monetary policy, by and large, coincide with the objectives of the overall economic policy. The broad objectives of monetary policy in India have been:

1) To maintain a reasonable degree of price stability

2) To ensure adequate expansion in credit to assist growth.

For the accomplishment of the aforesaid objectives, RBI uses various tools. Such tools are Cash Reserve Ratio (CRR), Statutory Liquidity Ratio (SLR), directed credit, Open Market Operation (OMO), etc.

Read Also – 10 Best Online Productivity Tools for Lawyers

Cash Reserve Ratio (CRR)

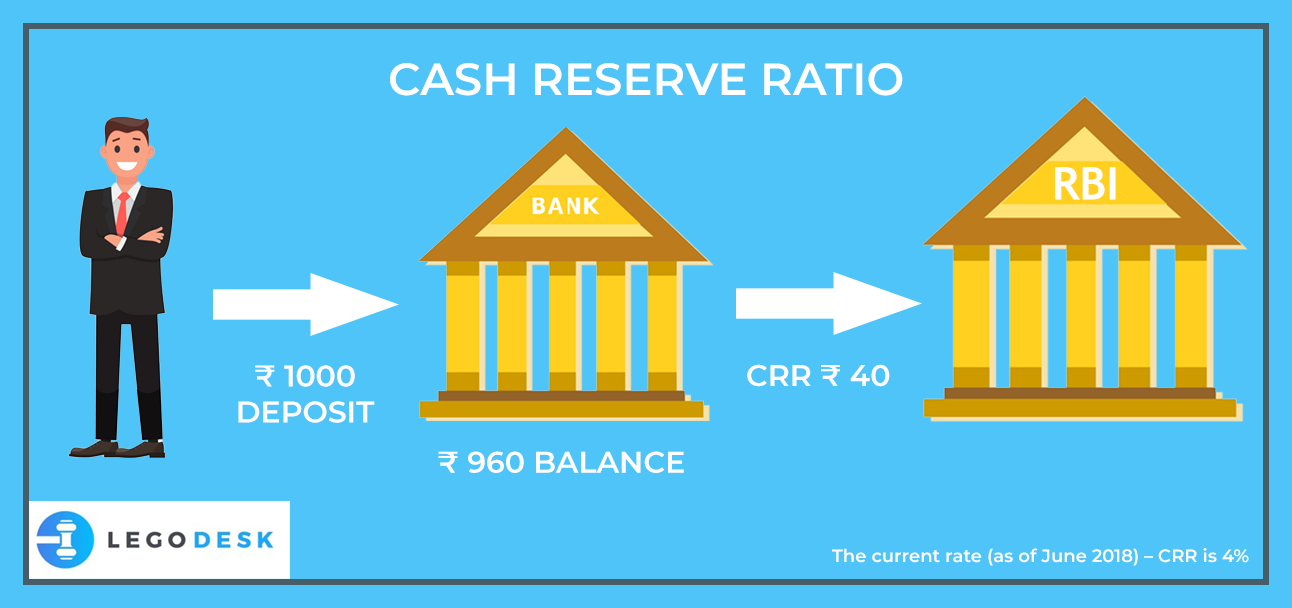

The cash reserve ratio refers to the cash which banks have to maintain with the Reserve Bank of India as a certain percentage of their demand and time liabilities.

Under the provision of the Reserve Bank of India Act, 1934, the scheduled commercial banks were required to maintain with the Reserve Bank every week a minimum of average daily cash reserve equivalent to three percent of their demand and time liabilities as an outstanding as on the Friday of the previous week. However, the Reserve Bank is empowered to vary the cash reserve ratio between three to fifteen percent. The current rate (as of June 2018) – CRR is 4%.

The RBI pays no interest on the amount of CRR to the Bank. Banks are bound to follow this regulation of CRR. It reflects the governing nature of RBI.

Read Also – Understanding the Civil Laws in India

Demand Liability

Liability of the bank to pay on demand is called Demand Liability. In other words, Demand Liabilities are those liabilities which are payable by the bank on the demand.

Example: Current Deposits, Demand Drafts, Cash Certificates etc.

Time Liability

Time liabilities are those liabilities of a bank which are payable otherwise on demand.

Example: Fixed Deposits, Staff Security Deposits, etc.

Read Also – What is Current Account

Net Demand Time Liability

Bank has some liabilities as aforesaid mentioned. Also, it has some deposits in other banks which are assets of the bank.

The aggregate sum of liabilities and assets of the bank is called Net Demand Time Liability of the Bank.

NDTL of a Bank = Demand and time liabilities (deposits) – deposits with other banks.

Read Also – Different Types of bond in India

Cash Reserve Ratio as a Tool

CRR is the ultimate tool for the purpose of saving a bank in its hard time. Every bank aims to earn a profit. For this purpose, banks wish to lend their maximum money in the market. Let’s assume a bank has Rs 100 crore in the balance sheet. For making the maximum profit it would like to lend all the money in the market. Thereafter the survival of the bank goes at risk. If the loan becomes NPA, it puts an adverse impact on the economy. Moreover, by lending all the money in the market, it increases the flow of money in the market. With this, the value of currency lessens. Further, it leads to ‘Price-inflation’.

Therefore, by putting the criteria of maintaining the CRR, The central bank achieve two goals;

Firstly, it saves the bank in a hard time. Secondly, it controls the flow of money in the market.

Altogether, the central bank can increase or decrease the percentage of CRR rate according to need. Permissible variation is from 3% to 15%. This variation enables the central bank to control the flow of money in the nation. When the market needs more supply of money, the rate of CRR can be reduced. Further, if the supply of money is high in the market, RBI can increase the CRR rate. Due to the increase in the CRR rate, the bank has lesser money to lend. 2% to 4% inflation is the ideal rate for the Indian Economy.

Conclusion

CRR is a monetary tool. Banks maintain with the central bank a certain sum of money i.e. CRR. Further, Central Bank uses it as a monetary tool to control the flow of money in the nation. When the central bank feels that price inflation is increasing, it increases the percentage of CRR. When the central bank sees the economy is moving towards depression, it reduces the CRR. This cash reserve is very helpful to the bank during the economic crisis.

In other words, for the benefit of the banks, Central Bank imposes some restriction as a guardian. CRR is one of the various restrictions (tool). Not to mention that maintaining the CRR with RBI is mandatory and not an option.