MSME Cash Credit – Navigating Financial Success with Dos and Don’ts

Micro, Small, and Medium Enterprises (MSMEs) play a vital role in the economic growth and development of any nation. To fuel their expansion and sustain their operations, MSMEs often require financial support, and one of the popular financing options available to them is “MSME Cash Credit.” This revolving credit facility allows MSMEs to draw funds from a predefined credit limit as per their working capital needs.

However, while MSME Cash Credit can be a valuable lifeline, it can also become a double-edged sword if not managed wisely. In this article, we will explore the dos and don’ts of utilizing MSME Cash Credit to help entrepreneurs navigate their financial journey successfully.

Understanding MSME Cash Credit

1. Definition and Purpose:

MSME Cash Credit is a type of working capital loan where financial institutions provide a credit limit based on the MSME’s turnover and creditworthiness. Entrepreneurs can withdraw funds as per their requirements, repay them, and reuse the facility. It helps MSMEs manage seasonal fluctuations, meet day-to-day operational expenses, and seize growth opportunities.

2. Eligibility Criteria:

Before availing MSME Credit, entrepreneurs should assess their eligibility based on factors such as credit score, business vintage, turnover, and financial health. A strong credit history and financial stability increase the chances of approval and favorable terms.

Dos before Availing MSME Cash Credit

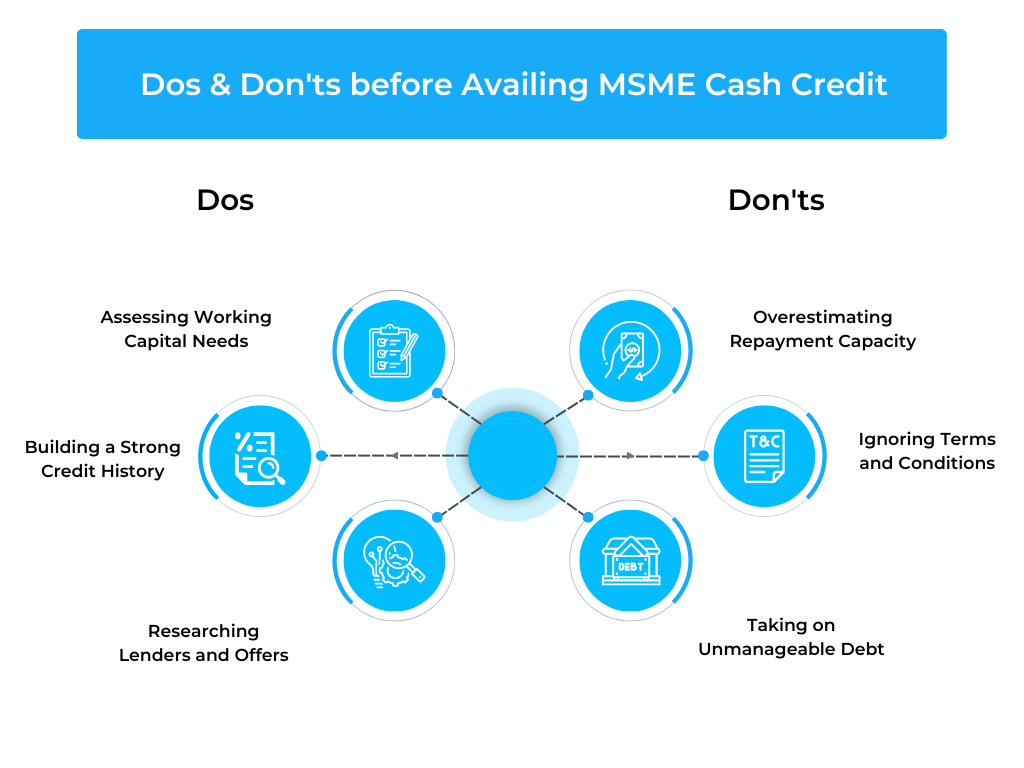

Assessing Working Capital Needs:

Before applying for MSME Credit, businesses should conduct a thorough analysis of their working capital requirements. Understanding the amount needed and the purpose of borrowing will prevent overborrowing and unnecessary interest costs.

Building a Strong Credit History:

Maintaining a positive credit history is crucial for obtaining the best terms and interest rates. Timely repayment of existing debts, trade credits, and prompt payment of dues can boost the credit profile.

Researching Lenders and Offers:

MSMEs should explore various lending institutions, compare interest rates, processing fees, and repayment terms. Choosing the right lender and offer can lead to significant cost savings in the long run.

Don’t when Applying for MSME Cash Credit

Overestimating Repayment Capacity:

While it is essential to meet working capital needs, overestimating the repayment capacity can lead to excessive borrowing. It may strain the business during lean periods, affecting the ability to repay on time.

Ignoring Terms and Conditions:

MSMEs must carefully read and understand the terms and conditions of the cash credit facility. Ignoring the fine print can lead to unexpected charges and penalties, causing financial strain.

Taking on Unmanageable Debt:

Entrepreneurs should not take on excessive debt without a clear plan for utilization and repayment. Uncontrolled borrowing can lead to a debt trap, jeopardizing the sustainability of the business.

Dos during MSME Cash Credit Utilization

Utilize Funds Wisely for Working Capital Needs:

Entrepreneurs should use the cash credit funds solely for working capital requirements, such as purchasing inventory, meeting payroll, or covering short-term expenses. This ensures that the borrowed funds are utilized effectively to generate revenue.

Maintain Proper Records and Bookkeeping:

Accurate bookkeeping is essential to monitor cash flow, track expenses, and assess the effectiveness of MSME Credit utilization. Proper records also facilitate smooth audits and compliance with regulatory requirements.

Regularly Monitor Cash Flow:

Consistent monitoring of cash flow helps entrepreneurs understand how effectively MSME Credit is meeting their working capital needs. It enables them to make timely adjustments to ensure financial stability.

Don’ts during MSME Cash Credit Utilization

Using Funds for Non-business Purposes:

Entrepreneurs should refrain from using cash credit funds for personal expenses or non-business activities. Mixing business and personal finances can lead to financial mismanagement and tax complications.

Ignoring Repayment Deadlines:

Timely repayment is critical for maintaining a healthy credit profile and fostering a positive relationship with the lender. Ignoring repayment deadlines can lead to penalties and impact future borrowing opportunities.

Failing to Communicate with the Lender:

In case of financial difficulties or unforeseen challenges, entrepreneurs should communicate proactively with the lender. Avoiding communication can create misunderstandings and hamper the possibility of finding mutually beneficial solutions.

Understanding Interest and Repayment

Interest Calculation Methods:

MSMEs must understand the various interest calculation methods used by lenders, such as reducing balance and flat rate. Comparing these methods can help them select the most cost-effective option.

Early Repayment Benefits and Penalties:

Some lenders offer incentives for early repayment, while others impose penalties for prepayment. Understanding these aspects can influence the decision to repay the cash credit before the scheduled tenure.

Dos for Managing MSME Cash Credit Effectively

Regularly Reviewing Financial Health:

MSMEs should periodically assess their financial health, monitor key performance indicators, and identify areas for improvement. This proactive approach enhances financial stability and growth prospects.

Exploring Credit Limit Increases:

As the business expands, MSMEs can request credit limit increases based on their improved financial performance. A higher credit limit provides greater financial flexibility during periods of growth.

Seeking Professional Financial Advice:

Entrepreneurs should consider seeking advice from financial experts or consultants to make informed decisions about borrowing, investment, and financial management.

Don’ts for Avoiding MSME Cash Credit Issues

Relying Solely on Cash Credit for Growth:

While MSME Cash Credit can be helpful, businesses should not solely rely on it for expansion. Diversifying funding sources and exploring other financial instruments can reduce risk and provide a more stable financial foundation.

Borrowing from Multiple Sources without a Plan:

Taking multiple loans without a well-defined plan can lead to cash flow issues and difficulty managing various repayment schedules. MSMEs should strategize their borrowing to ensure a smooth financial journey.

Overlooking Changes in Market Conditions:

Entrepreneurs must stay updated about market conditions, industry trends, and economic shifts. Ignoring these factors may result in cash flow disruptions and hinder the ability to manage cash credit effectively.

Conclusion: Navigating MSME Cash Credit Responsibly

In conclusion, MSME Credit can be a powerful financial tool when used responsibly and prudently. By following the dos and don’ts outlined in this article, entrepreneurs can harness the potential of cash credit to fuel growth, manage working capital efficiently, and achieve long-term financial success.

Remember, financial discipline, effective utilization, and proactive planning are the keys to success for MSMEs on their financial journey.