Avoiding Common Mistakes When Applying for MSME Credit

Micro, Small, and Medium Enterprises (MSMEs) play a pivotal role in driving economic growth and fostering entrepreneurship. However, access to credit has been a longstanding challenge for these small businesses.

To support their growth and sustainability, various financial institutions and governments offer MSME credit options tailored to their specific needs. Yet, many MSME owners make avoidable mistakes when applying for credit, leading to rejection or unfavorable loan terms.

In this article, we will explore some common mistakes made by MSMEs during the credit application process and provide actionable tips to avoid them.

Understanding the MSME Credit Landscape

Understanding the MSME credit landscape is crucial for small and medium-sized business owners seeking financial support to grow and expand their enterprises. MSME credit refers to the various financial products and services tailored specifically for Micro, Small, and Medium Enterprises (MSMEs).

These businesses play a significant role in driving economic growth, job creation, and innovation in many countries around the world.

Importance of MSME Credit:

- MSMEs often face financial constraints, limiting their ability to invest in new equipment, expand operations, or meet working capital requirements. MSME credit serves as a vital lifeline, providing the necessary funds to bridge the financial gaps and support growth.

- Access to credit empowers MSMEs to take advantage of market opportunities, diversify their products/services, and compete with larger enterprises.

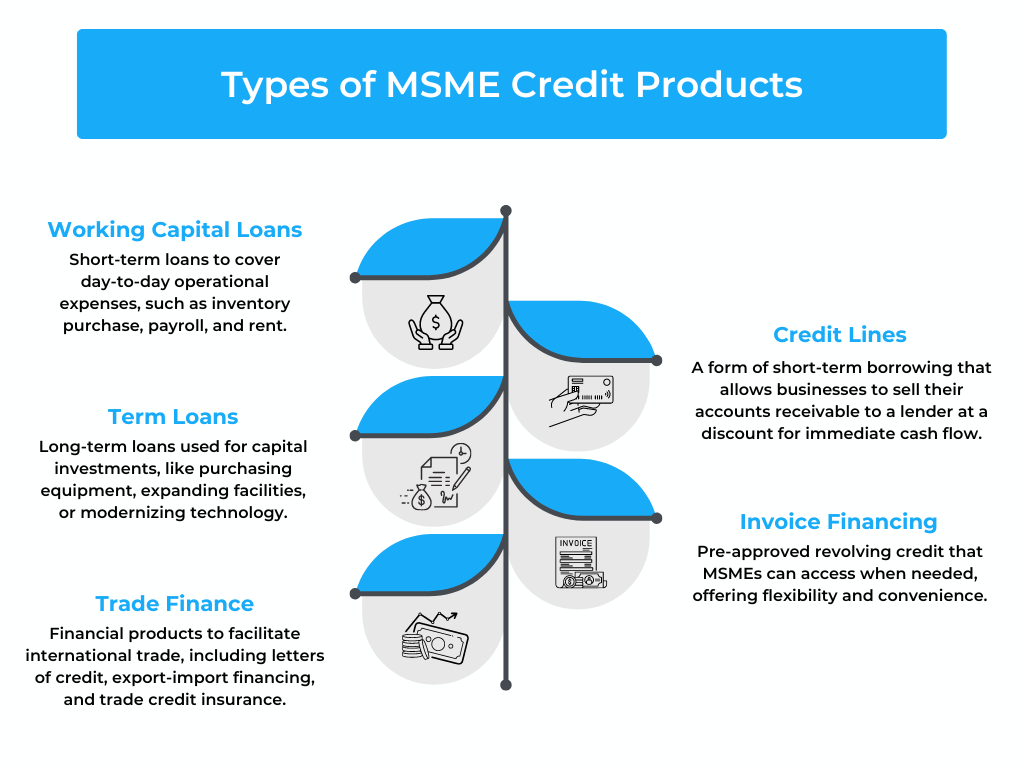

Types of MSME Credit Products:

- Working Capital Loans: Short-term loans to cover day-to-day operational expenses, such as inventory purchase, payroll, and rent.

- Term Loans: Long-term loans used for capital investments, like purchasing equipment, expanding facilities, or modernizing technology.

- Trade Finance: Financial products to facilitate international trade, including letters of credit, export-import financing, and trade credit insurance.

- Invoice Financing: A form of short-term borrowing that allows businesses to sell their accounts receivable to a lender at a discount for immediate cash flow.

- Credit Lines: Pre-approved revolving credit that MSMEs can access when needed, offering flexibility and convenience.

Eligibility Criteria for MSME Credit:

Different lenders may have varying eligibility criteria based on factors such as the business’s size, sector, credit history, and revenue.

In many cases, the business owner’s personal credit history and financial position may also be considered.

Government Initiatives and Support:

Governments in many countries often offer specific schemes and initiatives to promote MSME growth. These may include subsidized interest rates, collateral-free loans, and credit guarantees to reduce the risk for lenders.

MSMEs should explore and take advantage of such government-backed programs to access credit on favorable terms.

Challenges in Obtaining MSME Credit:

- MSMEs might face challenges in obtaining credit due to inadequate financial documentation, lack of credit history, or perceived higher risk by lenders.

- Collateral requirements can be a significant obstacle for businesses with limited assets to pledge.

Common mistakes made by MSMEs

Inadequate Financial Records

One of the most common mistakes MSME owners make is neglecting their financial records. Lenders heavily rely on these records to assess the creditworthiness of a business. Absent, incomplete, or poorly organized financial records can raise red flags and hinder the approval process.

To avoid this mistake, MSMEs must maintain accurate and up-to-date financial statements, including profit and loss statements, balance sheets, and cash flow reports. Using accounting software can streamline this process and provide lenders with a clear picture of the business’s financial health.

Overlooking Credit Score and History

MSMEs often underestimate the importance of their credit score and history when applying for credit. A strong credit history demonstrates the business’s ability to manage debts and repay loans promptly. Lenders consider this information to assess the credit risk associated with the borrower.

A low credit score or a history of defaults can lead to higher interest rates or outright loan rejection. Therefore, MSME owners must regularly monitor their credit score, resolve any discrepancies, and proactively work towards improving it.

Unrealistic Loan Amount Request

Another common mistake is requesting an unrealistic loan amount. While it may be tempting to secure a large sum to address various business needs, lenders prefer applications that demonstrate a clear and specific purpose for the requested funds.

MSME owners must conduct a thorough assessment of their financial requirements and apply for a loan amount that aligns with their immediate needs and repayment capacity. A well-defined loan purpose and a realistic repayment plan can increase the chances of loan approval.

Ignoring Diverse Lending Options

Many MSMEs limit their options by approaching only traditional banks for credit. In today’s financial landscape, numerous alternative lenders, online lending platforms, and government-backed initiatives provide credit options specifically designed for MSMEs.

These alternative sources often offer competitive interest rates, flexible terms, and faster processing times. MSME owners must explore various lending options and choose the one that best suits their business needs.

Lack of a Comprehensive Business Plan

A comprehensive business plan is a vital tool that showcases the MSME’s vision, mission, growth strategy, and financial projections. It provides lenders with insights into the business’s potential for success and how the loan will contribute to its growth.

Many MSMEs make the mistake of applying for credit without a well-structured business plan, which can be detrimental to their chances of securing the loan. Having a clear and realistic business plan not only enhances credibility but also instills confidence in lenders about the borrower’s ability to manage the funds responsibly.

Applying for Multiple Loans Simultaneously

Desperation to secure funds may lead MSME owners to apply for multiple loans simultaneously. However, this approach can backfire as lenders view multiple credit applications within a short span as a sign of financial distress and increased credit risk.

Each loan application generates a hard inquiry on the credit report, which negatively impacts the credit score. Instead, MSMEs should carefully assess their needs, identify the most suitable lending option, and apply strategically to avoid potential negative consequences.

Insufficient Collateral or Guarantees

Many lenders require collateral or personal guarantees to secure MSME credit. Owners often make the mistake of providing inadequate or inappropriate collateral, leading to rejection or unfavorable terms.

MSMEs must be cautious about pledging valuable assets and should explore alternative collateral options that align with the loan amount and terms. Additionally, seeking guidance from financial advisors or industry experts can help MSME owners make informed decisions regarding collateral or guarantees.

Conclusion

Access to credit is a critical factor in the growth and sustenance of MSMEs. Avoiding common mistakes during the credit application process can significantly enhance the chances of loan approval and favorable terms. MSME owners must prioritize financial record-keeping, maintain a strong credit score, and have a well-defined business plan to impress lenders.

Furthermore, exploring diverse lending options, applying for realistic loan amounts, and providing appropriate collateral can help establish the credibility and reliability of the business. By learning from these mistakes and adopting proactive strategies, MSMEs can secure the credit they need to thrive and contribute to the economic ecosystem.