All about Credit Card Delinquency

Credit cards are a popular and convenient way to purchase and manage finances. From a lender’s perspective, credit card delinquency can result in financial losses and damage their reputation. From a user’s perspective, it can lead to fees, damage to credit score, and difficulty obtaining credit in the future.

In this article, we will explore from both a lender’s and a user’s perspective. We will discuss what it is, the consequences of delinquency for both parties, and strategies for avoiding and managing it. Whether you are a lender or a credit card user, this article will provide valuable insights into the world of credit card delinquency.

Read More: 7 Attorney Business Cards Rules

What is Credit Card Delinquency?

Credit card delinquency refers to the failure of a credit card holder to make timely payments on their credit card account. This can happen for various reasons, including financial difficulties or simply forgetting to make a payment. Delinquency can have severe consequences for the cardholder, including damage to their credit score and the possibility of legal action by the credit card company.

It can occur due to a variety of reasons, such as financial hardship, overspending, or simply forgetting to make the payment on time. Also, credit card delinquency can have significant consequences for both the credit card issuer and the account holder. In the following sections, we will explore these consequences in more detail.

Consequences of Credit Card Delinquency for Lenders

Some of the consequences of it for lenders are as follows:

Financial Losses:

When credit card account holders become delinquent, credit card issuers may incur financial losses. This is because they may not receive the interest and fees that the account would otherwise generate. In addition, if the delinquency continues, the issuer may have to write off the account as a loss, which can impact their bottom line.

Damage to Reputation:

Credit card delinquency is a serious problem that can have significant consequences for both the cardholder and the credit card issuer. Delinquency can result in damage to the cardholder’s credit score and legal action by the credit card company. Furthermore, suppose a large number of account holders become delinquent. In that case, it can damage the reputation of the credit card issuer, leading to a decrease in the issuer’s stock price and a decrease in the number of new customers applying for their credit cards. To mitigate these consequences, credit card issuers may take steps to prevent delinquency, such as monitoring accounts for early signs of financial difficulty, offering payment plans and other options to manage debt, and pursuing collections activity if the delinquency continues.

Read Also: All About Aadhaar Card and Common Problems

Consequences of Credit Card Delinquency for Users

Some of the consequences of it for users are as follows:

Fees and Penalties:

It can result in fees and penalties for the account holder. These fees can include late payment fees, over-limit fees, and increased interest rates. They can add up quickly, making it even more difficult for the account holder to pay off their balance.

Damage to Credit Score:

It can also have a negative impact on the account holder’s credit score. Late payments and delinquency can stay on the credit report for up to seven years, which can make it more difficult to obtain credit in the future. A lower credit score can also result in higher interest rates on loans and credit cards, making it more expensive to borrow money.

Difficulty Obtaining Credit:

Credit card delinquency can make it harder to get credit in the future. Lenders see delinquent accounts as risky and may reject credit applications from those with a history of delinquency.

To avoid this, users should make timely payments, keep balances low, and monitor credit reports often. If an account becomes delinquent, communication with the issuer and establishing a payment plan are important to prevent further harm to credit scores and finances.

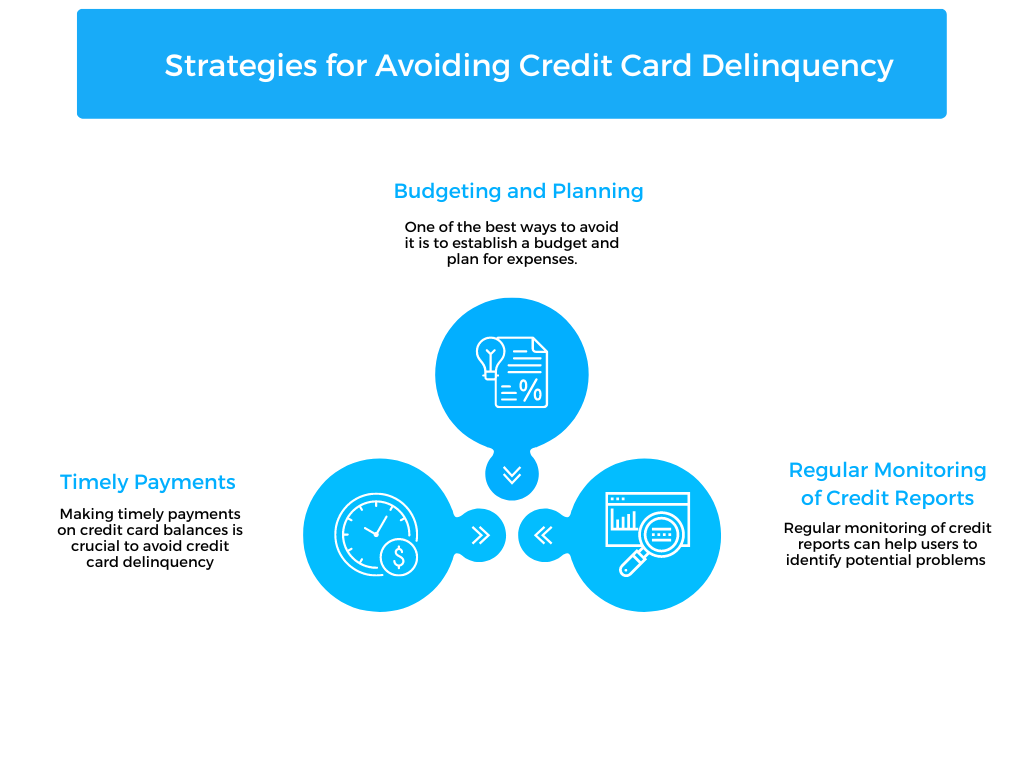

Strategies for Avoiding Credit Card Delinquency

By implementing these strategies, credit card users can avoid it and maintain healthy credit habits.

Budgeting and Planning:

One of the best ways to avoid it is to establish a budget and plan for expenses. This can help users to manage their spending and avoid overspending on their credit cards. Creating a budget involves assessing one’s income and expenses, setting financial goals, and allocating funds accordingly. This can help users to avoid using their credit cards to make purchases they cannot afford, which can lead to credit card delinquency.

Timely Payments:

Making timely payments on credit card balances is crucial to avoid credit card delinquency. Users should make payments on time, at least the minimum payment required by the issuer, and avoid missing or making late payments. This can help users to avoid fees, penalties, and damage to their credit score.

Regular Monitoring of Credit Reports:

Regular monitoring of credit reports can help users to identify potential problems before they become significant issues. Users should check their credit reports regularly to ensure that they are accurate and up-to-date. Any errors or inaccuracies should be reported to the credit bureau as soon as possible. Additionally, monitoring credit reports can help users to identify any delinquencies or missed payments and take corrective action before they become significant issues.

Strategies for Managing Credit Card Delinquency

By implementing these strategies, credit card users can effectively manage credit card delinquency and take steps to avoid further damage to their credit score and financial well-being.

Communication with Lenders:

One of the most critical strategies for managing credit card delinquency is to communicate with the credit card issuer. If a user anticipates that they may have difficulty making their payment, they should contact the issuer to explain the situation and discuss options for resolving the issue. In some cases, the issuer may be willing to work with the user to establish a payment plan or other arrangements to help them avoid delinquency.

Negotiation of Payment Terms:

Users who are experiencing credit card delinquency may also consider negotiating payment terms with their credit card issuer. This can involve working out a payment plan that is more manageable for the user, such as a lower interest rate or a more extended payment period. It is important to note that negotiation may not always be successful, but it is worth trying before resorting to other options.

Seeking Professional Assistance:

Credit card delinquency may sometimes be a symptom of a more significant financial problem. Users who are struggling to manage their debt and finances may consider seeking professional assistance, such as credit counseling or debt management services. These services can help users to develop a plan for paying off their debts and managing their finances more effectively.

Conclusion

Credit card delinquency can have serious consequences for both lenders and users. For lenders, it can result in financial losses and damage to reputation. At the same time, for users, it can lead to fees and penalties, damage to credit scores, and difficulty obtaining credit in the future. However, there are strategies for both avoiding and managing it.

Credit card users can maintain healthy credit habits and avoid the negative consequences of credit card delinquency. It is important to remember that it is not a hopeless situation, and with proactive management and communication, users can overcome their financial challenges and maintain good credit standing.