An Analysis of the MSME Credit Gap

The MSME credit gap is the difference between the amount of credit that MSMEs need and the amount of credit that they are able to access. It is a major challenge for MSMEs around the world, as it prevents them from growing and creating jobs.

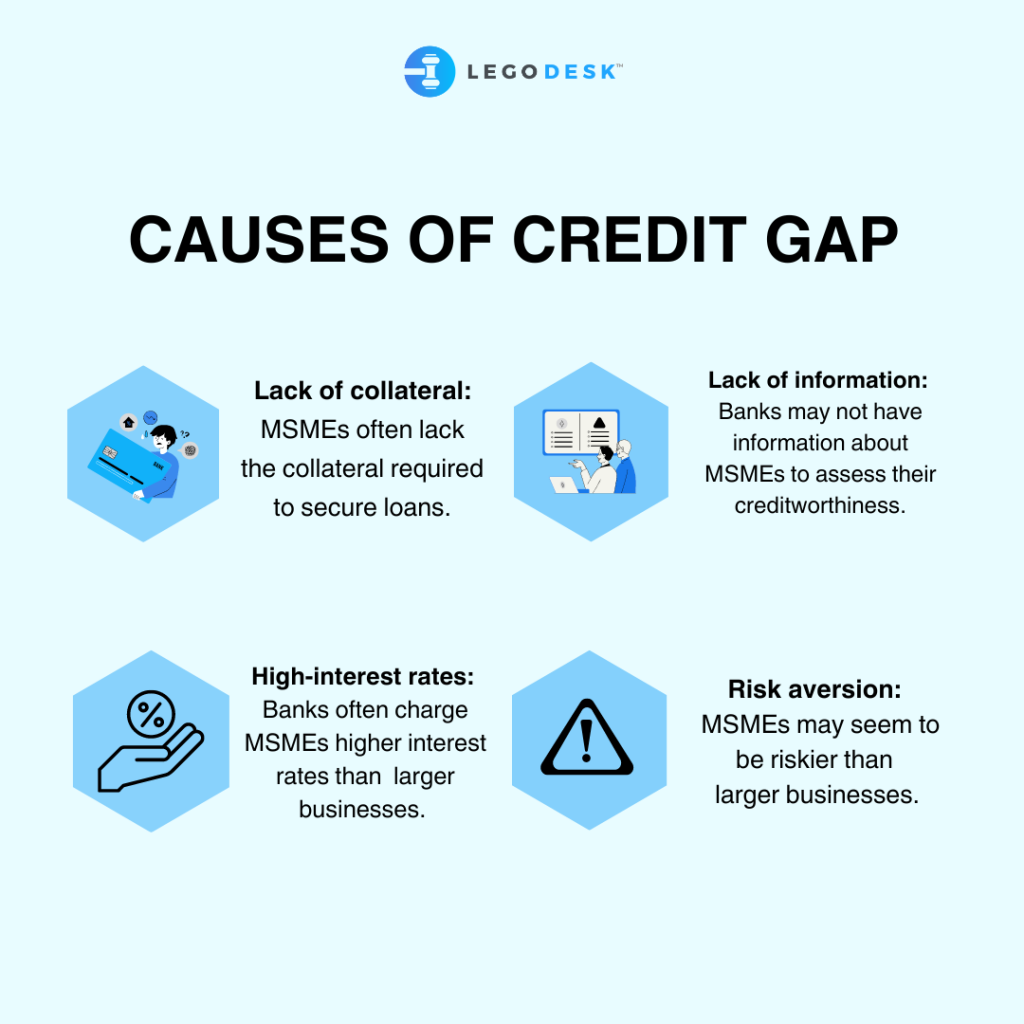

Causes of the MSME credit gap

There are a number of factors that contribute to the MSME credit gap, including:

- Lack of collateral: MSMEs often lack the collateral that banks require to secure loans.

- High-interest rates: Banks often charge MSMEs higher interest rates than they charge larger businesses.

- Lack of information: Banks may not have enough information about MSMEs to assess their creditworthiness.

- Risk aversion: Banks may be reluctant to lend to MSMEs because they perceive them to be riskier than larger businesses.

Impact of the MSME credit gap

The MSME credit gap has a number of negative impacts, including:

- It prevents MSMEs from growing and creating jobs.

- It can lead to MSMEs closing down.

- It can reduce competition in the market.

- It can increase inequality.

Solutions to the MSME credit gap

There are a number of solutions to the MSME credit gap, including:

- Providing MSMEs with access to collateral: This can be done through government-backed schemes or through partnerships between banks and MSMEs.

- Reducing interest rates: This can be done by the government or by banks themselves.

- Providing MSMEs with information: This can be done through government-backed schemes or through banks themselves.

- Reducing risk aversion: This can be done by the government or by banks themselves.

Causes of the MSME credit gap

The MSME credit gap is the difference between the amount of credit that MSMEs need and the amount of credit that they are able to obtain from formal financial institutions. The causes of the MSME credit gap can be divided into two categories: demand-side factors and supply-side factors.

Demand-side factors include:

- Lack of collateral: MSMEs often lack the collateral that banks require in order to secure a loan.

- High-interest rates: MSMEs often have to pay higher interest rates than larger businesses.

- Lack of financial literacy: MSMEs may not be aware of the available financing options or may not be able to understand the terms of a loan.

Supply-side factors include:

- Risk aversion: Banks may be reluctant to lend to MSMEs because they perceive them as being riskier than larger businesses.

- Lack of competition: In some markets, there may be a lack of competition among banks, which can lead to higher interest rates and less availability of credit.

- Lack of data: Banks may not have enough data on MSMEs to assess their creditworthiness.

The MSME credit gap has a number of negative consequences, including:

- It can hinder the growth of MSMEs.

- It can lead to job losses.

- It can reduce innovation.

- It can exacerbate inequality.

There are a number of things that can be done to address the MSME credit gap, including:

- Providing government guarantees for loans to MSMEs.

- Developing credit scoring models for MSMEs.

- Increasing competition in the banking sector.

- Providing financial education to MSMEs.

Impact of the MSME credit gap

The MSME credit gap is the difference between the amount of credit that MSMEs need and the amount of credit that they are able to obtain from formal financial institutions. This gap can have a significant impact on the growth and development of MSMEs, as well as on the overall economy.

The MSME credit gap can be caused by a number of factors, including:

- Lack of collateral: MSMEs often lack the collateral that banks require in order to secure a loan.

- High-interest rates: MSMEs often have to pay higher interest rates than larger businesses, which can make it difficult for them to afford loans.

- Lack of information: MSMEs may not have access to information about the availability of credit or the terms and conditions of loans.

- Risk aversion: Banks may be reluctant to lend to MSMEs because they perceive them as being riskier investments than larger businesses.

The impact of the MSME credit gap can be significant. MSMEs that are unable to obtain credit may be forced to scale back their operations or even close down. This can lead to job losses and a decrease in economic activity. In addition, the MSME credit gap can hinder the development of new businesses and technologies.

There are a number of things that can be done to address the MSME credit gap. These include:

- Providing MSMEs with access to collateral: This can be done through government-backed programs or through partnerships between banks and MSMEs.

- Reducing interest rates: Governments can provide subsidies or tax breaks to banks that lend to MSMEs.

- Increasing access to information: Governments and banks can work together to provide MSMEs with information about the availability of credit and the terms and conditions of loans.

- Reducing risk aversion: Governments can provide guarantees or insurance to banks that lend to MSMEs.

By taking these steps, governments and banks can help to close the MSME credit gap and support the growth and development of MSMEs.

Solutions to the MSME credit gap

There are a number of solutions that can be implemented to address the MSME credit gap. These include:

- Strengthening the financial sector: This includes measures to improve access to finance for MSMEs, such as developing credit bureaus, improving the regulatory environment, and providing training to financial institutions on lending to MSMEs.

- Providing targeted credit guarantees: This involves providing guarantees to lenders against losses on loans to MSMEs, which can help to reduce the risk of lending to this segment.

- Promoting alternative finance: This includes measures to promote the development of alternative finance providers, such as crowdfunding and peer-to-peer lending, which can provide MSMEs with access to finance that they may not be able to obtain from traditional banks.

- Supporting business development services: This includes providing MSMEs with access to business development services, such as training, mentoring, and market research, which can help them to improve their performance and access finance.

- Encouraging entrepreneurship: This includes measures to encourage entrepreneurship, such as providing training and support to entrepreneurs and developing a culture of entrepreneurship.

These are just some of the solutions that can be implemented to address the MSME credit gap. By implementing a combination of these solutions, it is possible to improve access to finance for MSMEs and help them to grow and create jobs.

Conclusion

In conclusion, it is important to stay up-to-date on current trends and what is popular in order to be successful in business. By keeping an eye on what our customers are looking for, we can ensure that we are always offering the products and services that they want. This will help us to stay ahead of the competition and continue to grow our business.

Try our Debt Resolution solutions today Request a Demo