Microguide to dispute settlement for banks

Disputes are an unfortunate but inevitable part of doing business, and the banking industry is no exception. Banks must be prepared to handle disputes that arise with customers, vendors, and other third parties. A well-crafted dispute resolution process can not only help resolve disputes quickly and efficiently, but it can also improve the overall customer experience and protect the bank’s reputation. In this microguide, we will explore the key elements of an effective dispute settlement process for banks, including legal considerations, best practices for dispute management, and tips for communicating with customers during the process. Whether you are a bank employee or a customer, this guide will provide valuable insights on how to navigate disputes in the banking industry.

Legal considerations for bank disputes

Some of the legal considerations for bank disputes are as follows:

Regulatory compliance: Banks are subject to a wide range of laws and regulations that govern their operations, and disputes that arise with customers or vendors may implicate these rules. Banks must ensure that their dispute resolution process is compliant with relevant laws, such as the Truth in Lending Act, the Fair Credit Reporting Act, and the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Contractual obligations: Banks often enter into agreements with customers and vendors that contain specific dispute resolution provisions. These provisions may dictate the process for resolving disputes, the venue for any legal proceedings, and the applicable law. Banks must be familiar with the dispute resolution provisions in their contracts and ensure that they are following the process outlined in the agreement.

Limitations of liability: Banks may be able to limit their liability in the event of a dispute by using contracts, agreements, or other legal documents. Banks should review these documents to ensure that they are properly protecting themselves from potential liability.

Alternative dispute resolution: Banks may opt to use alternative dispute resolution (ADR) methods, such as arbitration or mediation, to resolve disputes. ADR can be less formal and less expensive than traditional litigation and maybe a more efficient way to resolve disputes. Banks should consider the benefits and limitations of ADR methods when developing their dispute resolution process.

Data protection and privacy: Banks handle a significant amount of personal data and financial information, and disputes may arise related to data protection and privacy. Banks should be familiar with the relevant data protection laws, such as the General Data Protection Regulation (GDPR) in the European Union and the California Consumer Privacy Act (CCPA) in the US.

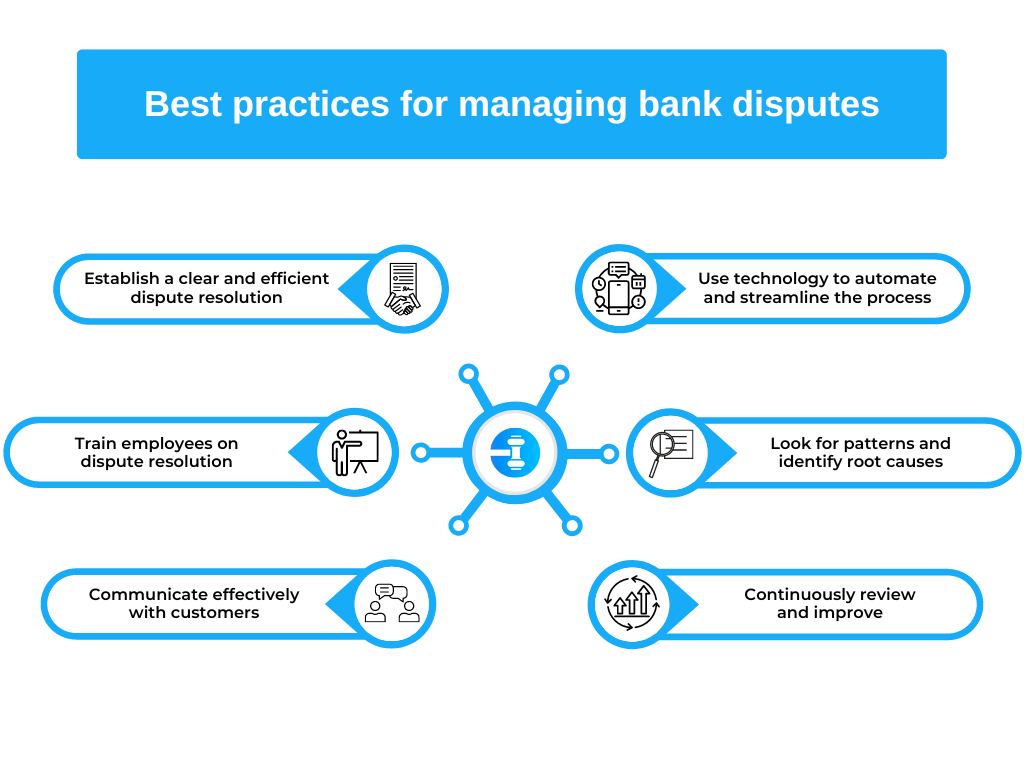

Best practices for managing bank disputes

Given below are the best practices for managing bank disputes in an efficient and effective manner:

Establish a clear and efficient dispute resolution process: Banks should have a clear and efficient process in place for handling disputes. This process should be well-documented, easy to understand, and accessible to employees and customers. The process should also include clear timelines for resolution and regular reviews to ensure that it is functioning effectively.

Train employees on dispute resolution: Banks should ensure that employees are properly trained on the bank’s dispute resolution process and how to handle disputes effectively. This training should include information on how to communicate with customers during a dispute and how to document the dispute resolution process.

Communicate effectively with customers: Effective communication is key to managing bank disputes. Banks should ensure that they are providing clear and timely information to customers about the dispute resolution process and the status of their complaints. Banks should also be sensitive to the customer’s concerns and work to address them in a timely and respectful manner.

Use technology to automate and streamline the process: Banks can use technology to automate and streamline their dispute resolution process. This can include using customer relationship management (CRM) systems to track and manage disputes, using data analytics to identify patterns in disputes, and using online portals to allow customers to submit complaints and track the status of their disputes.

Look for patterns and identify root causes: Banks should look for patterns in disputes and try to identify the root causes of the disputes. This can help banks to address underlying issues and prevent similar disputes from arising in the future.

Continuously review and improve: Banks should continuously review and improve their dispute settlement process. This can include gathering feedback from customers and employees, measuring the effectiveness of the process, and making changes as needed to improve the process.

Communication strategies for addressing customer complaints

With effective communication strategies, banks can address customer complaints in a timely and respectful manner, build trust with customers, and increase their satisfaction with the resolution of complaints.

Listen actively: Banks should actively listen to customers when they raise complaints and try to understand their concerns. This can involve asking clarifying questions, paraphrasing the customer’s concerns, and acknowledging the customer’s feelings.

Be empathetic: Banks should approach customer complaints with empathy and try to put themselves in the customer’s shoes. This can involve acknowledging the customer’s frustration and working to address their concerns in a timely and respectful manner.

Be transparent: Banks should be transparent with customers about the dispute settlement process and the status of their complaints. Banks should provide clear and timely information to customers about the next steps in the process and what they can expect in terms of a resolution.

Keep customers informed: Banks should keep customers informed about the status of their complaints and any actions that are being taken to resolve them. Banks should also provide regular updates to customers and set realistic expectations for the resolution of the complaint.

Apologize and take responsibility: Banks should apologize for any mistakes or issues that have led to the complaint and take responsibility for resolving the issue. This can help to build trust with the customer and make them more likely to be satisfied with the resolution of the complaint.

Follow-up: Banks should follow up with customers after the complaint has been resolved to ensure that they are satisfied with the resolution and to identify any areas for improvement. This can help to prevent similar complaints from arising in the future.

Conclusion and next steps for improving your bank’s dispute settlement process

In conclusion, disputes are an unfortunate but inevitable part of doing business, and the banking industry is no exception. Banks must be prepared to handle disputes that arise with customers, vendors, and other third parties. A well-crafted dispute resolution process can not only help resolve disputes quickly and efficiently, but it can also improve the overall customer experience and protect the bank’s reputation.

To improve your bank’s dispute resolution process, it is essential to establish a clear and efficient process, train employees on dispute resolution, communicate effectively with customers, use technology to automate and streamline the process, look for patterns and identify root causes, and continuously review and improve the process.

To take the next steps in improving your bank’s dispute resolution process, you can start by conducting a review of your current process, gathering feedback from customers and employees, and identifying areas for improvement. You may also consider implementing new technologies, such as CRM systems and online portals, to automate and streamline the process. Finally, it may be beneficial to provide additional training and education to employees on how to handle disputes effectively and communicate with customers during a dispute. By taking these steps, your bank can improve its dispute resolution process, increase customer satisfaction, and reduce the risk of disputes arising in the future.

Additional resources for bank dispute resolution

Some additional resources for bank dispute resolution include government agencies such as the Consumer Financial Protection Bureau (CFPB) and the Federal Reserve, as well as organizations such as the Better Business Bureau (BBB) and the National Association of Consumer Advocates (NACA). Additionally, consulting with a financial advisor or attorney may also be helpful.