The Impact of Debt on Your Credit Score and How to Improve It

In today’s world, credit scores play a critical role in our financial lives. Your credit score is a numerical representation of your creditworthiness. It affects your ability to obtain credit. Examples of credit include loans, credit cards, and mortgages. One of the factors that significantly impact your credit score is the amount of debt you have.

In this article, we will explore the impact of debt on your credit score and discuss some practical strategies to improve it. You may be struggling with different forms of debt such as credit card debt or student loans. It’s important to understand the impact that debt has on your credit score. Taking steps to improve your credit score can have a significant impact on your financial well-being.

Understanding Credit Score and Debt

A credit score is a numerical value that represents an individual’s creditworthiness. It is based on their credit history and credit report, which contains information about their borrowing and repayment habits. Lenders commonly use credit scores to make loan or credit decisions. Credit scores help lenders determine whether to approve a loan or credit application. They also help set the interest rate for the loan or credit.

There are several credit scoring models, but the most commonly used is the FICO score, which ranges from 300 to 850. The higher the score, the better the creditworthiness of the individual. A good credit score is generally considered to be 700 or above.

Types of Debt That Affect Credit Score:

There are two main types of debt that can affect an individual’s credit score: revolving debt and installment debt.

Revolving debt is debt that does not have a fixed repayment term, such as credit cards. The credit limit is the maximum amount that an individual can borrow. They are free to borrow as much or as little as they want up to the credit limit. The amount owed on revolving debt is reported to credit bureaus each month, and a high balance can negatively impact credit scores.

An installment debt is a debt that has a fixed repayment term, such as car loans and mortgages. The amount owed on installment debt is reported to credit bureaus each month, and making payments on time can help improve credit scores.

How Credit Utilization Ratio Affects Credit Score:

Credit utilization ratio refers to the amount of revolving debt an individual has compared to their total credit limit. For example, if an individual has a credit card with a $10,000 limit and a balance of $5,000, their credit utilization ratio is 50%.

A high credit utilization ratio can have a negative impact on credit scores. This is because it suggests that the individual may be relying too heavily on credit. It could also indicate potential difficulty in paying back the borrowed amount. Experts generally recommend keeping credit utilization below 30% to maintain a good credit score.

Other Factors That Affect Credit Score:

Several other factors can impact an individual’s credit score, including:

- Payment history: Late payments or missed payments can have a significant negative impact on credit scores.

- Length of credit history: A longer credit history is generally viewed more favorably by lenders.

- Credit mix: Having a mix of revolving debt and installment debt can positively impact credit scores.

- New credit: Applying for multiple new credit accounts within a short period of time can negatively impact credit scores. This is because it suggests that the individual may be taking on too much debt too quickly.

How Debt Affects Credit Score

One of the most significant factors that can negatively impact a credit score is missed or late payments. When payments are missed or made late, it suggests that the borrower may be having difficulty managing their debts and paying bills on time. Late payments can stay on a credit report for up to seven years. The negative impact of a late payment on a credit score can increase the longer the payment is past due.

Another way that debt can impact credit scores is through the debt-to-income (DTI) ratio. The DTI ratio is the amount of debt an individual has compared to their income. If an individual has a high DTI ratio, it suggests that they may have difficulty making their debt payments on time, which can negatively impact their credit score. Generally, a DTI ratio of 36% or less is considered good, while a ratio of 50% or higher is considered poor.

When an individual is unable to make their debt payments, their account may be sent to a debt collection agency. Debt collection accounts can have a significant negative impact on credit scores, as they indicate that the individual has defaulted on their debt. The amount of the debt and how long it has been delinquent can also impact the severity of the negative impact on the credit score. Debt collection accounts can remain on a credit report for up to seven years, even after the debt has been paid off.

How to Improve Your Credit Score

Improving a credit score can be a daunting task, but there are several strategies that can help individuals achieve this goal. Here are some ways to improve a credit score:

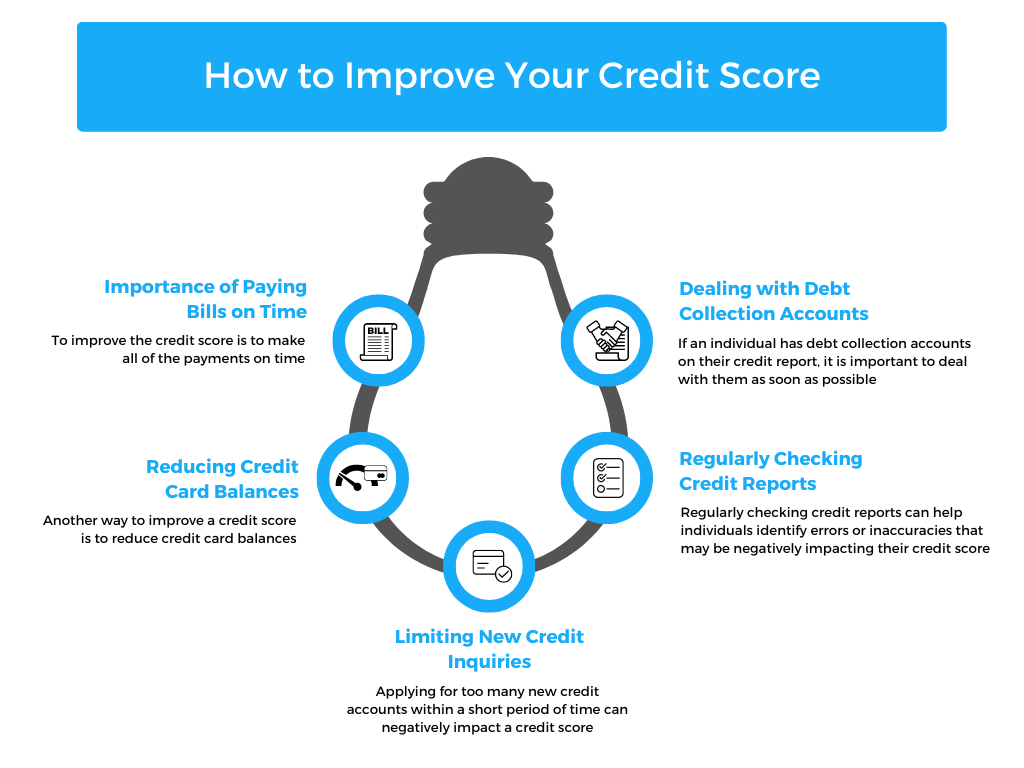

A. Importance of Paying Bills on Time:

One of the most important things an individual can do to improve their credit score is to make all of their payments on time. This includes credit card payments, loan payments, and utility bills. Late payments can have a significant negative impact on credit scores and can take several years to recover from.

B. Reducing Credit Card Balances:

Another way to improve a credit score is to reduce credit card balances. A high credit card balance can negatively impact a credit score, especially if the credit utilization ratio is high. Experts generally recommend keeping credit card balances below 30% of the credit limit to maintain a good credit score.

C. Limiting New Credit Inquiries:

Applying for too many new credit accounts within a short period of time can negatively impact a credit score. This is because it suggests that the individual may be taking on too much debt too quickly. To improve a credit score, it is important to limit new credit inquiries and only apply for credit when necessary.

D. Regularly Checking Credit Reports:

Regularly checking credit reports can help individuals identify errors or inaccuracies that may be negatively impacting their credit score. If an error is found, it can be disputed with the credit bureau to have it corrected.

E. Dealing with Debt Collection Accounts:

If an individual has debt collection accounts on their credit report, it is important to deal with them as soon as possible. Paying off the debt can help improve the credit score. If paying off the debt in full is not possible, negotiating a payment plan with the collection agency may be an option to consider. It is also important to ensure that the debt collection account is removed from the credit report once it has been paid off or settled.

Strategies for Managing Debt

Debt management is an essential part of improving a credit score and achieving financial stability. Here are some strategies for managing debt:

A. Developing a Budget:

Developing a budget is an important step in managing debt. A budget can help individuals understand their income and expenses and identify areas where they can reduce spending. By sticking to a budget, individuals can ensure that they have enough money to make their debt payments on time and avoid incurring new debt.

B. Exploring Debt Consolidation Options:

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate. This can make it easier for individuals to manage their debt and make their payments on time. There are several debt consolidation options available, such as balance transfer credit cards, personal loans, and home equity loans. It is important to research these options carefully and choose the one that is most suitable for one’s financial situation.

C. Seeking Professional Help for Debt Management:

If an individual is struggling to manage their debt, seeking professional help may be necessary. Credit counseling agencies can provide advice on budgeting, debt consolidation, and debt management strategies. Debt management companies can negotiate with creditors to lower interest rates and create a payment plan that is affordable for the individual. However, it is important to research these companies carefully and choose a reputable one that has a good track record.

Conclusion

In conclusion, having a good credit score is essential for achieving financial stability and accessing credit at favorable terms. Managing debt responsibly is key to improving a credit score and avoiding financial pitfalls. By developing a budget, exploring debt consolidation options, and seeking professional help, individuals can manage their debt effectively and improve their credit scores. It is important for readers to take action to improve their credit scores and educate themselves on similar topics by reading informative content on platforms like Legodesk.