The Impact of Microfinance on Rural Economy and Challenges in Recovery

Introduction to Microfinance in Rural Areas

Microfinance has emerged as a powerful tool for fostering inclusive economic growth and addressing financial exclusion in rural areas. It encompasses a range of financial services, including microcredit, savings, insurance, and payment systems, tailored to meet the specific needs of low-income individuals and underserved communities. In rural areas, where traditional banking infrastructure is often scarce, microfinance plays a crucial role in providing access to financial services and empowering individuals to improve their livelihoods.

In many rural economies, a significant portion of the population lacks access to formal banking services. This exclusion can limit their ability to save, invest, and access credit, thereby constraining economic opportunities. Microfinance institutions (MFIs) have stepped in to bridge this gap by offering small loans and financial services to rural communities, particularly to entrepreneurs, smallholder farmers, and women who face additional barriers to accessing financial resources. By promoting financial inclusion, microfinance has the potential to stimulate rural economies, generate income, and alleviate poverty in these areas.

Positive Impact of Microfinance on Rural Economy

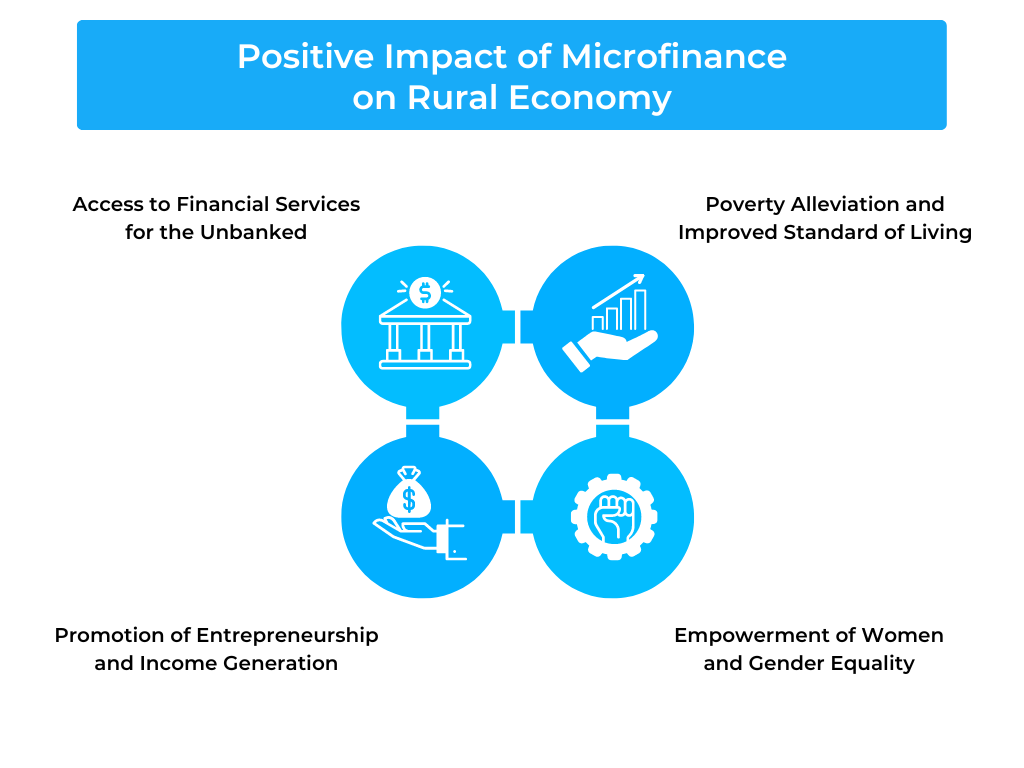

Microfinance has demonstrated a range of positive impacts on rural economies, bringing about transformative changes in the lives of individuals and communities. The following key areas highlight the positive effects of microfinance in rural areas:

- Access to Financial Services for the Unbanked: Microfinance provides an avenue for the unbanked population in rural areas to access financial services. This access to credit, savings, and insurance enables individuals to invest in income-generating activities, smooth consumption patterns, and build assets. By empowering individuals with financial tools, microfinance unlocks their economic potential and contributes to the growth of rural economies.

- Promotion of Entrepreneurship and Income Generation: Microfinance plays a vital role in fostering entrepreneurship in rural areas. By providing small loans and business training, it enables aspiring entrepreneurs to start or expand their microenterprises. This access to capital and technical support stimulates economic activity, creates employment opportunities, and contributes to local economic growth.

- Poverty Alleviation and Improved Standard of Living: Microfinance has been successful in reducing poverty and improving living conditions in rural areas. By providing financial resources, individuals can invest in education, healthcare, housing, and other essential needs. Increased incomes and improved living standards have a ripple effect on the overall well-being of rural communities.

- Empowerment of Women and Gender Equality: Microfinance has been instrumental in empowering women in rural areas. By granting them access to financial services, women can establish their businesses, generate income, and gain economic independence. This economic empowerment contributes to reducing gender inequalities, promoting women’s decision-making power, and enhancing their social status within their communities.

Enhancing Agricultural Productivity through Microfinance

Microfinance plays a critical role in enhancing agricultural productivity and driving rural development by providing tailored financial services to farmers and agricultural enterprises. The following factors demonstrate how microfinance contributes to the growth and sustainability of the agricultural sector:

- Provision of Agricultural Loans and Inputs: Microfinance institutions offer agricultural loans to farmers, enabling them to invest in seeds, fertilizers, machinery, and other inputs necessary for agricultural production. These loans help farmers improve their production capabilities, adopt modern farming techniques, and enhance their overall productivity.

- Development of Value Chains and Market Linkages: Microfinance facilitates the development of agricultural value chains by providing financial support to various actors involved, such as farmers, processors, aggregators, and distributors. By strengthening these linkages, microfinance enables farmers to access wider markets, obtain fair prices for their produce, and increase their income. This, in turn, promotes agricultural productivity and encourages investment in the sector.

- Skill Development and Training Programs: Microfinance institutions often complement their financial services with training programs and capacity-building initiatives for farmers. These programs enhance farmers’ knowledge and skills in areas such as sustainable farming practices, post-harvest management, marketing strategies, and financial management. By equipping farmers with the necessary skills, microfinance contributes to improved agricultural productivity and profitability.

Microfinance’s role in enhancing agricultural productivity goes beyond financing. It also encompasses the provision of knowledge, resources, and support systems that empower farmers to make informed decisions and adopt sustainable agricultural practices. Through these comprehensive approaches, microfinance strengthens the agricultural sector, promotes food security, and contributes to the overall economic growth of rural areas.

Microfinance Challenges in Rural Economic Recovery

While microfinance has shown significant potential in driving rural economic recovery, there are several challenges that need to be addressed to maximize its effectiveness. The following challenges highlight the obstacles faced in leveraging microfinance for rural economic recovery:

- Limited Access to Capital and Funding: Microfinance institutions often struggle with limited access to capital and funding sources, especially in rural areas. This hinders their ability to provide sufficient financial resources to meet the demand for loans and other financial services. Lack of capital can slow down the pace of economic recovery, as it restricts the ability of rural entrepreneurs and farmers to invest in their businesses and agricultural activities.

- Lack of Financial Literacy and Business Management Skills: Many individuals in rural areas have limited financial literacy and lack basic business management skills. This poses challenges in effectively utilizing microfinance services and making informed financial decisions. Inadequate understanding of interest rates, loan terms, and financial planning can lead to overindebtedness and mismanagement of funds, hindering economic recovery efforts.

- Geographical and Infrastructural Constraints: Rural areas often face geographical and infrastructural constraints that impact the delivery of microfinance services. Limited physical infrastructure, such as roads and communication networks, can impede the accessibility of financial services in remote rural areas. The cost of reaching scattered populations may also pose challenges for microfinance institutions, making it difficult to establish and maintain operations.

- Adapting to Climate Change and Environmental Factors: Rural economies heavily rely on agriculture, which is vulnerable to climate change and environmental factors. Extreme weather events, droughts, and changing rainfall patterns can affect agricultural productivity and disrupt loan repayments. Microfinance institutions need to factor in these risks and develop climate-resilient financial products and risk management strategies to support rural economic recovery.

Innovative Solutions and Best Practices in Microfinance

Microfinance institutions (MFIs) are continually evolving and implementing innovative solutions and best practices to overcome challenges and maximize their impact in rural areas. The following are examples of innovative approaches and best practices in microfinance:

- Digital Financial Inclusion and Mobile Banking: MFIs are leveraging technology to expand financial inclusion in rural areas through digital financial services. Mobile banking platforms and digital payment systems enable individuals to access financial services conveniently, even in remote areas. This approach reduces transaction costs, improves efficiency, and promotes financial access for the unbanked population.

- Peer-to-Peer Lending and Group Savings: Peer-to-peer lending models, where individuals within a community contribute to a common fund and lend to each other, have gained popularity in microfinance. This approach fosters social capital, builds trust, and ensures financial resources circulate within the community, promoting entrepreneurship and local economic development. Similarly, group savings initiatives encourage individuals to save collectively, strengthening financial resilience and providing a source of internal capital for community members.

- Impact Investing and Social Entrepreneurship: Impact investors play a crucial role in supporting microfinance institutions and their clients. By providing capital with a social and environmental mission, impact investors promote sustainable development and support the growth of microfinance. Additionally, microfinance institutions are increasingly fostering social entrepreneurship by providing not only financial services but also business development support, mentorship, and networking opportunities to aspiring entrepreneurs.

- Public-Private Partnerships and Collaboration: Collaboration between microfinance institutions, governments, NGOs, and private sector entities is vital for sustainable microfinance operations. Public-private partnerships help leverage resources, share knowledge, and create an enabling environment for microfinance. Governments can support microfinance through favorable policies, regulatory frameworks, and capacity-building initiatives, while private sector entities bring in expertise, technology, and funding.

Policy and Regulatory Framework for Microfinance

The policy and regulatory framework for microfinance plays a crucial role in shaping the operations and impact of microfinance institutions (MFIs) in rural areas. An effective and supportive framework provides a conducive environment for the growth and sustainability of microfinance. The following aspects highlight the key components of a robust policy and regulatory framework for microfinance:

Supportive Government Policies and Regulations: Governments play a critical role in creating an enabling environment for microfinance. They can develop and implement policies that promote financial inclusion, encourage microfinance activities, and protect the rights of microfinance clients. Governments can also establish regulatory bodies to oversee the operations of microfinance institutions, ensure compliance with regulations, and safeguard the interests of borrowers.

Microfinance Institutions and Regulatory Bodies: Clear guidelines and regulations for the establishment, licensing, and operation of microfinance institutions are essential. Regulatory bodies should be empowered to monitor the performance and integrity of MFIs, including their financial stability, governance practices, and client protection measures. Regular audits, inspections, and reporting requirements can help maintain transparency and accountability within the microfinance sector.

Consumer Protection and Client Safeguarding: Policies and regulations should prioritize the protection of microfinance clients. Measures can include setting fair interest rate ceilings, ensuring transparent loan terms and conditions, and prohibiting exploitative practices. Clear disclosure requirements, grievance mechanisms, and mechanisms for resolving disputes should be established to protect the rights and interests of borrowers.

Conclusion:

Microfinance has shown promise in driving rural economy recovery by providing access to financial services, promoting entrepreneurship, enhancing agricultural productivity, and empowering individuals. Overcoming challenges such as limited access to capital, financial literacy gaps, infrastructural constraints, and climate change risks is crucial. Through innovative solutions like digital financial inclusion and peer-to-peer lending, collaborative partnerships, and a supportive policy framework, microfinance can continue to play a vital role in fostering sustainable and inclusive rural economic development.