Debt restructuring and transfer of loan exposures: Best practices for banks and financial institutions

In the world of finance, debt restructuring and transfer of loan exposures are common practices used by banks and financial institutions to manage their risks and improve their financial health.

These practices involve the modification of existing loans or the transfer of loan obligations to other institutions, which can be complex and challenging processes. To ensure that these practices are executed effectively and efficiently, it is essential for banks and financial institutions to follow best practices and guidelines.

In this article, we will explore the best practices for debt restructuring and transfer of loan exposures, including their benefits, challenges, and key considerations that banks and financial institutions need to keep in mind.

Understanding Debt Restructuring and Transfer of Loan Exposures

Debt restructuring and transfer of loan exposures are financial practices used by banks and financial institutions to manage their credit risk and optimize their loan portfolios. Debt restructuring involves the modification of existing loan terms and conditions to make them more favorable for borrowers and reduce the risk of default. This can include changes to interest rates, repayment terms, or the overall amount of debt owed.

- Transfer of loan exposures, on the other hand, involves the sale or assignment of loans to another financial institution or investor. This can be done through securitization or syndication, where the loans are packaged together and sold to investors as securities.

- Alternatively, loans can be sold directly to another financial institution or transferred to a special purpose vehicle (SPV) for management.

- Both debt restructuring and transfer of loan exposures are used by banks and financial institutions to manage their risk exposure and optimize their capital allocation.

- By restructuring loans or transferring them to other institutions, banks can reduce their exposure to risky borrowers or industries, while also freeing up capital for other lending activities.

However, these practices can be complex and require careful planning and execution to be successful.

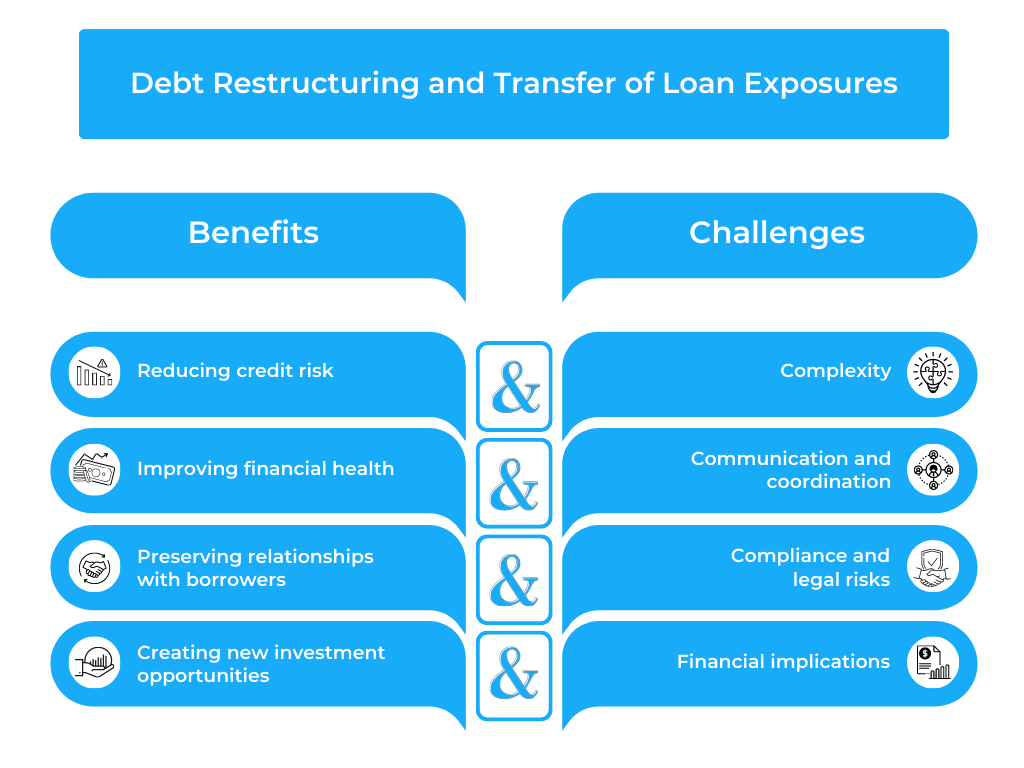

Benefits and Challenges of Debt Restructuring and Transfer of Loan Exposures

Benefits

Reducing credit risk: Debt restructuring and transfer of loan exposures can help banks and financial institutions reduce their credit risk by managing their exposure to high-risk borrowers or industries.

Improving financial health: By restructuring loans or transferring them to other institutions, banks can improve their financial health and optimize their capital allocation, which can help them remain competitive in the market.

Preserving relationships with borrowers: Restructuring loans can help banks maintain relationships with their borrowers by providing them with financial relief and avoiding defaults.

Creating new investment opportunities: Transfer of loan exposures can create new investment opportunities for investors looking to diversify their portfolio or gain exposure to specific industries or regions.

Challenges

Complexity: Debt restructuring and transfer of loan exposures can be complex processes that require extensive knowledge of financial instruments, legal frameworks, and regulatory requirements.

Communication and coordination: Effective communication and coordination with borrowers, investors, and other stakeholders are crucial to the success of these practices. Miscommunication or lack of coordination can lead to delays or even failure.

Compliance and legal risks: Debt restructuring and transfer of loan exposures must comply with regulatory and legal requirements, which can be challenging and time-consuming to navigate. Non-compliance can result in legal and reputational risks.

Financial implications: Restructuring loans or transferring loan exposures can have financial implications for both the bank and the borrower. The bank may need to write off some of the loan principal, while the borrower may face additional fees or higher interest rates.

Best Practices for Debt Restructuring and Transfer of Loan Exposures

Conducting a Comprehensive Assessment of the Borrower’s Financial Condition:

Before restructuring loans or transferring loan exposures, banks and financial institutions should conduct a thorough assessment of the borrower’s financial condition. This includes reviewing the borrower’s financial statements, cash flow projections, and business plans to determine their ability to repay the loan. The assessment should also consider any changes in the borrower’s industry or market conditions that may impact their ability to repay the loan.

Developing a Clear Restructuring and Transfer Strategy

Banks and financial institutions should develop a clear strategy for debt restructuring and transfer of loan exposures that aligns with their overall business objectives. The strategy should include a detailed plan for the restructuring or transfer, including the timeline, the terms of the new loan, and the roles and responsibilities of all stakeholders.

The strategy should also identify any potential risks or challenges and outline contingency plans to mitigate them.

Communication and Collaboration with Borrowers and Other Stakeholders

Effective communication and collaboration with borrowers and other stakeholders are essential to the success of debt restructuring and transfer of loan exposures. Banks and financial institutions should be transparent about their intentions and engage in ongoing dialogue with borrowers to ensure their needs and concerns are addressed.

Collaboration with other stakeholders, such as investors, regulators, and legal advisors, can also help ensure compliance with regulatory and legal requirements.

Compliance with Regulatory and Legal Requirements

Debt restructuring and transfer of loan exposures must comply with regulatory and legal requirements. Banks and financial institutions should conduct due diligence to ensure compliance with applicable laws and regulations, including anti-money laundering (AML), know-your-customer (KYC), and data protection laws.

It is also important to engage legal advisors with expertise in debt restructuring and transfer of loan exposures to ensure compliance with legal requirements and avoid legal and reputational risks.

Assessing the Cost and Benefits

Banks and financial institutions should also assess the cost and benefits of debt restructuring and transfer of loan exposures. This includes analyzing the financial impact of the restructuring or transfer on both the borrower and the institution.

The cost analysis should include any fees associated with the restructuring or transfer, as well as any potential losses or gains resulting from changes to the loan terms. The benefits analysis should consider the potential for reduced credit risk, improved financial health, and new investment opportunities.

Implementing Robust Risk Management Practices

Effective risk management practices are critical to the success of debt restructuring and transfer of loan exposures. Banks and financial institutions should establish clear policies and procedures for managing credit risk, including underwriting standards, loan monitoring, and risk reporting.

They should also implement strong internal controls and oversight mechanisms to ensure compliance with regulatory and legal requirements and mitigate operational risks.

Conclusion

Debt restructuring and transfer of loan exposures are important tools for banks and financial institutions to manage credit risk and optimize their capital allocation. However, these practices can be complex and challenging, requiring extensive knowledge of financial instruments, legal frameworks, and regulatory requirements.

Effective communication and collaboration with borrowers and other stakeholders, compliance with regulatory and legal requirements, and robust risk management practices are key to the success of debt restructuring and transfer of loan exposures.

Future Outlook

As the banking industry continues to evolve, it is likely that debt restructuring and transfer of loan exposures will become even more important for managing credit risk and optimizing capital allocation. Advances in technology, such as blockchain and machine learning, may also enable banks and financial institutions to streamline and automate these processes, improving efficiency and reducing costs.

However, as with any new technology, it will be important to ensure compliance with regulatory and legal requirements and maintain strong risk management practices to mitigate operational risks.

Try our Debt Resolution solutions today Request a Demo