What to do if your client’s cheque bounced?

In this development of the financial world, we see many cases these days relating to default of payment through cheques. The pendency of cheque bounce cases is also rising daily in India. People approach lawyers so that they can help them with the available legal recourses related to this subject matter. Therefore, as a lawyer, you must understand these terms and what legal remedies you can use to protect the interest of your client.

What is a cheque bounce?

Cheque is a Negotiable Instrument through which one party promises to pay a certain amount of money to another party on the specific mentioned date. Cheque bounce or cheque dishonoured is a state in which the person who promises to pay the amount is unable to pay on a such specific date. When any cheque is presented before the bank and that cheque is bounced then a banker must return the cheque with a “cheque return memo”. A cheque return memo is basically a document that shows the reason for why the cheque is returned unpaid. A cheque can be bounced for any reason such as a signature mismatched, a cheque presented after the expiration period, Insufficiency of funds in a bank account, Payment stopped by the account holder, etc.

Protection of cheque bounce cases under Indian Law

Cheque bounce is a criminal offense and is punishable in India. The interest of every citizen whose cheque is bounced is protected under Section 138 of the Negotiable Instrument Act, of 1881. As per this Section, any person whose cheque is bounced for insufficiency of funds will be punished with imprisonment of 2 years or with a fine of double the cheque amount or with both.

To prosecute someone under this Section, these requirements should be fulfilled

- Cheque should be presented before the bank within six months from the date on which it is drawn. In the case of a post-dated cheque, it should be presented before the expiration period.

- Demand notice has to be sent to the defaulting party within 30 days from the acknowledgment of the cheque return memo from the bank.

- The defaulter fails to make the payment even after 15 days of serving demand notice.

Also, where the defaulter is a Company, the protection is given under Section 141 of the Negotiable Instrument Act 1881. In the case of the defaulter as a company, its directors and individuals will be liable. All those involved at the time of default will be prosecuted in the same manner as per section 138 of the Negotiable Instrument Act of 1881.

Exception:

In all the cases of cheque bounce due to insufficient funds, we can prosecute the defaulter under this Section. However, if the cheque was for a gift, donation, or any other obligation that is not legally enforceable cannot be prosecuted under this Section. This section will attract only debt due or discharge of legally enforced liability.

Now that you’re well aware of what these terms are and the remedies available to your client let’s understand step by step procedure you can follow to help your client:

First Step: Sending demand Notice

The first step involves sending a demand notice to prosecute the defaulter under Section 138. Gather the following information from your client: the defaulter’s full name and address, nature of the transaction, due amount, date of cheque bounce, etc., and daft a legal notice demanding payment within 15 days. Also, reference Section 138 of the NI Act and state that if the price is not made within 15 days, you are filing a criminal complaint against him. The primary purpose of this notice is to send the defaulter a warning about the consequences of non-payment. Ensure that the information you are sending is within the limitation period as per Section 138, i.e., 30 days from receiving the cheque return memo from the bank.

Second step: Filing Criminal Complaint

15 days after serving the demand notice, you can proceed with a criminal complaint if the defaulter still does not issue any fresh cheque or make the payment. A criminal complaint can be filed in the court of a magistrate within 30 days of the expiry of 15 days of serving of demand notice. There is a strict rule concerning the limit of 30 days, however, in case there is sufficient cause for delay the magistrate may accept the complaint even after the expiration of 30 days period.

Jurisdiction of Court

You can file a complaint in a court where the local jurisdiction where any of the incidences happened:

- Where the cheque was drawn

- Where cheque was presented

- Where the bank returned the cheque

- A place where demand notice was served to the defaulter

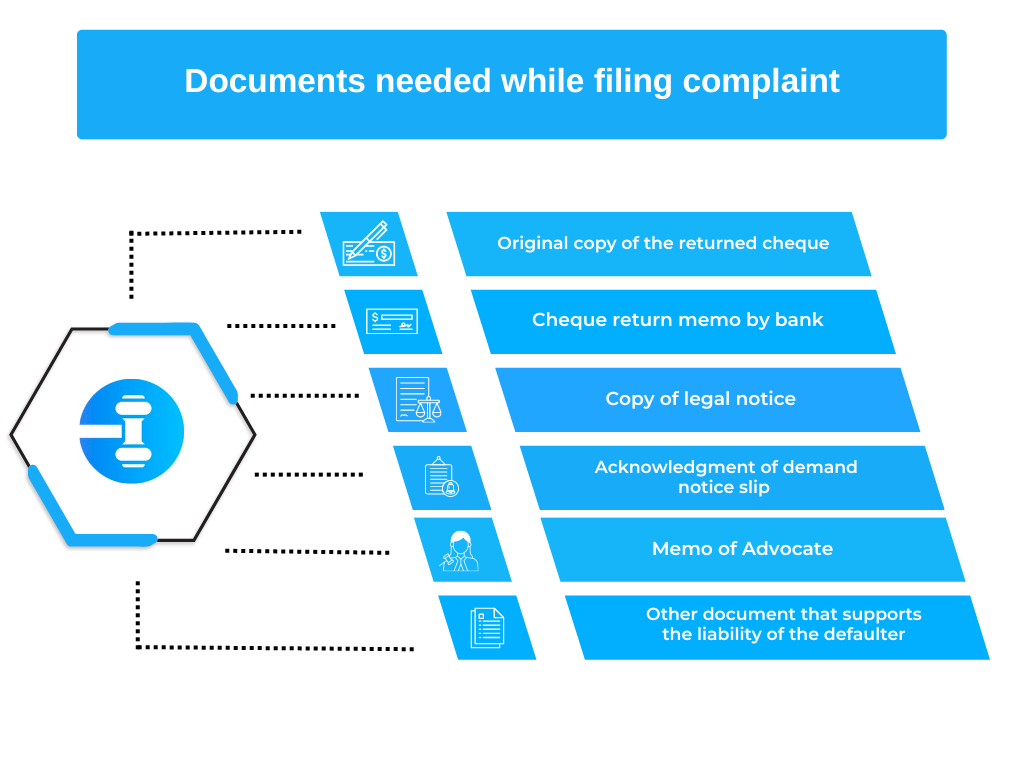

Required Documents

The following documents need to be attached while filing the complaint:

- Original copy of the returned cheque

- Cheque return memo by bank

- Copy of legal notice

- Acknowledgment of demand notice slip or receipt

- Memo of Advocate (popularly understandable as Vakalatnama)

- Any other document that supports the liability of the defaulter

After the complaint is filed, the court will issue summon to the defaulter, asking him to present before the court on the specified date. The court will hear the matter from both sides. If the court finds the accused guilty of the offense, he will be liable for the criminal charges.

If the defaulter fails to appear before the court on that specified day, the court can issue a bailable warrant against him. Where the accused still does not present himself before the court, the court can issue a non-bailable warrant of arrest against him.

Third Step: Filing of Civil Suit

Meanwhile, you also have the option to file a civil suit against the defaulter. This summary suit will help your client recover the money and the cost of litigation. This suit can be filed per order XXXVII of the Code of Civil procedure, 1908. The summary suit is different from the ordinary suit. It can be filed to recover the due amount of bills of exchange and promissory notes or in cases where there are written contracts to make payment. According to the summary procedure, the accused don’t have the right to defend themselves. They need permission from the court to protect themselves.

Conclusion

These above steps will help you to recover the amount from the defaulter through the judicial process. It is also essential to note that the Reserve Bank of India (RBI) has also laid down some rules to help decrease cheque defaults. Account holders must maintain a minimum cheque balance, and a penalty amount must be paid if the cheque bounces. You can also advise your client to report the case to credit information companies, which will affect the defaulter’s CIBIL Score. Though the legal system is clogged with cheque bounce cases, using these measures will help people protect their payment.

Try our Debt Resolution solutions today Request a Demo