Cheque Bounce Intimation Failure: What Happens Next and How to Avoid It

1. Introduction

Cheques are a widely accepted mode of payment in business transactions. But sometimes, they can bounce due to insufficient funds, signature mismatch or other reasons. It is crucial to understand what happens when a cheque bounces, the consequences of cheque bounce intimation failure and how to avoid it.

A cheque bounce intimation is a notice sent by the bank to the issuer of the cheque when the cheque is returned unpaid. The cheque bounce intimation typically includes information about the bounced cheque, the reason for the bounce, and the date and time of the bounce.

Cheque bounce can lead to legal action and damage to the reputation of the issuer. Therefore, it is essential to know the steps to handle such situations effectively. This article provides valuable insights on cheque bounce, cheque bounce intimation failure, and how to avoid them. Whether you are a business owner or an individual, understanding these concepts can help you manage your finances better.

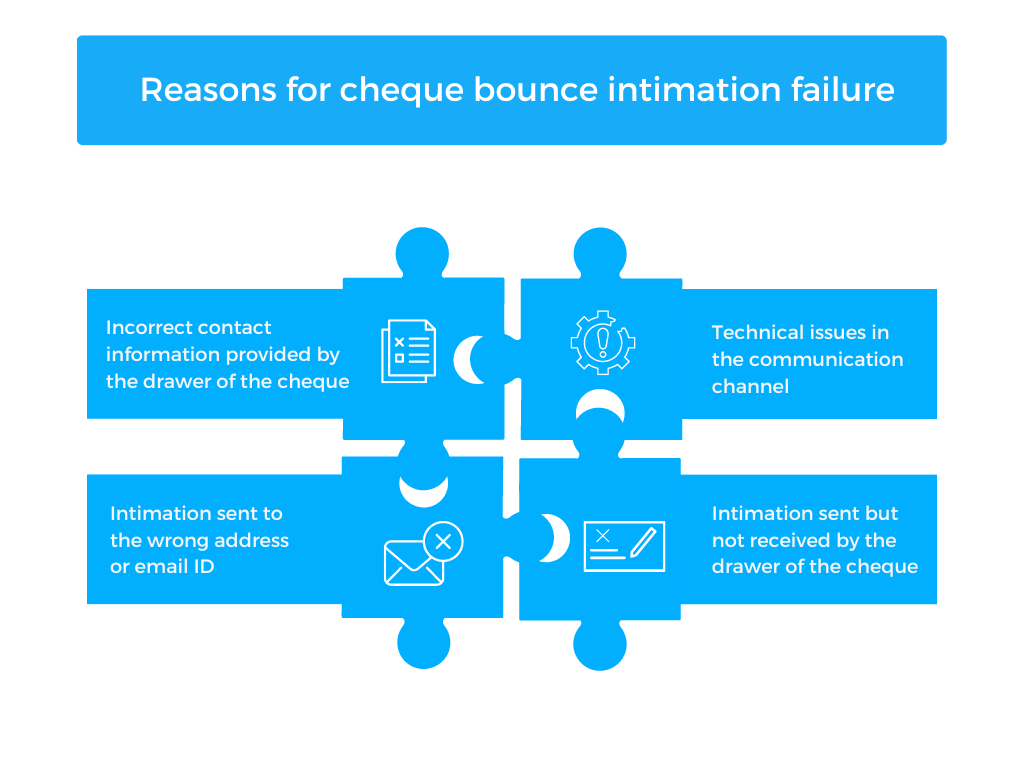

2. Reasons for cheque bounce intimation failure

There are cases when the intimation fails to reach the drawer of the cheque, which can result in further complications. Some of the common reasons for cheque bounce intimation failure are explained below:

Incorrect contact information provided by the drawer of the cheque:

The contact information provided by the drawer of the cheque, such as the address, phone number, or email ID, may be incorrect or outdated. This can lead to the intimation being sent to the wrong person or not being delivered at all.

Intimation sent to the wrong address or email ID:

There can be instances where the intimation is sent to the wrong address or email ID. It can be either due to a typo or a mistake made by the bank or the courier company. In such cases, the intimation fails to reach the drawer of the cheque, which can result in delays in resolving the issue.

Technical issues in the communication channel:

Sometimes, technical issues such as network problems, server downtime, or email delivery issues can cause the intimation to fail. This can happen due to factors beyond the control of the bank or the drawer of the cheque, and it can be difficult to identify the root cause of the problem.

Intimation sent but not received by the drawer of the cheque:

Even if the intimation is sent to the correct address or email ID, there may be instances where the drawer of the cheque does not receive it due to various reasons such as spam filters, email forwarding issues, or mailbox full errors.

3. Consequences of cheque bounce intimation failure

If the intimation fails to reach the drawer of the cheque, it can have several consequences, including:

Legal action: If the payee of the cheque or the bank decides to take legal action against the drawer of the cheque, the failure of the intimation can be used as evidence that the drawer was aware of the bounced cheque but failed to take corrective action.

Additional penalties and charges: If the drawer of the cheque fails to respond to the intimation and take corrective action, the bank may levy additional penalties and charges for the bounced cheque, including penalty fees, interest charges, and legal fees.

Impact on credit score: If the bounced cheque and subsequent penalties and charges are not resolved, it can have a negative impact on the credit score of the drawer of the cheque. This can make it difficult for the individual to obtain loans, credit cards, and other financial products in the future.

4. Legal provisions for cheque bounce

- Explanation of Section 138 of the Negotiable Instruments Act

The key provisions of Section 138 of the Negotiable Instruments Act are:

- The cheque must have been issued for the discharge of any debt or liability.

- The cheque must have been returned unpaid by the bank due to insufficient funds or any other reason.

- The payee must have given notice in writing to the drawer of the cheque demanding payment within 30 days of the receipt of the intimation regarding the dishonour of the cheque.

- The drawer must have failed to make the payment within 15 days of receipt of the notice.

- Punishments and penalties for cheque bounce

- Imprisonment for a term which may extend up to two years

- A fine which may extend up to twice the amount of the cheque or both

- The payee can file a complaint in court within 30 days of the cheque bounce

- The complaint should be in writing and contain necessary details such as the name of the issuer and the bank where the cheque was issued

- If the issuer is found guilty, they may be ordered to pay compensation to the payee

- The court may also order the issuer to pay the amount of the cheque along with interest to the payee

- Repeat offenders may face higher punishments and penalties.

- Steps to be taken in case of cheque bounce

- Inform the issuer of the bounced cheque and ask for a resolution

- Send a legal notice to the issuer demanding payment within 15 days

- If payment is not made within 15 days, file a complaint in court within 30 days of the cheque bounce

- The complaint should be in writing and contain necessary details such as the name of the issuer and the bank where the cheque was issued

- Attend court hearings and provide necessary evidence to prove the case

- If the issuer is found guilty, they may be ordered to pay compensation to the payee and may face punishments and penalties under the Negotiable Instruments Act, 1881

- If the issuer fails to pay the amount ordered by the court, the payee can file for recovery proceedings or initiate criminal proceedings to recover the amount.

5. Importance of responding to cheque bounce intimation

- Consequences of ignoring the intimation

- Ignoring the intimation can lead to legal action being taken against the issuer.

- The issuer may face penalties and punishments under the Negotiable Instruments Act, 1881.

- It can also harm the issuer’s reputation and credit score.

- Legal action that can be taken against the drawer of the cheque

- The payee can file a complaint in court against the issuer of the cheque within 30 days of the cheque bounce.

- The issuer can be punished with imprisonment or a fine under the Negotiable Instruments Act, 1881.

- The court may also order the issuer to pay compensation to the payee.

- Ways to resolve the issue after receiving the intimation

- The issuer can make the payment to the payee to resolve the issue.

- The issuer can request the payee for more time to make the payment.

- The issuer and the payee can enter into a settlement agreement to resolve the issue outside of court.

6. Steps to be taken after cheque bounce intimation failure

Contacting the payee or the bank to verify the status of the intimation:

If the issuer has not received any intimation about the cheque bounce, they should contact the payee or the bank to verify the status of the intimation.

Taking corrective action to update the contact information with the bank:

If the contact information provided to the bank is incorrect or outdated, the issuer should take corrective action to update their contact information with the bank to avoid missing any future intimation.

Exploring legal options to resolve the issue and prevent further penalties:

If the issuer has missed the opportunity to respond to the intimation and legal action has been taken against them, they should explore legal options to resolve the issue and prevent further penalties. This may include seeking legal advice, negotiating a settlement with the payee, or filing an appeal in court.

7. Ways to avoid cheque bounce intimation failure

Here are the ways to avoid cheque bounce intimation failure:

- Providing accurate and up-to-date contact information to the bank: It is important to provide accurate and up-to-date contact information, such as email address and phone number, to the bank to ensure that any intimation regarding the cheque bounce is received in a timely manner.

- Regularly checking and updating the contact information with the bank: It is also important to regularly check and update the contact information with the bank to avoid missing any intimation due to outdated or incorrect contact information.

- Ensuring that sufficient funds are available in the account to avoid cheque bounce: It is important to ensure that there are sufficient funds available in the account before issuing a cheque to avoid a cheque bounce. One should regularly monitor the account balance to ensure that it is sufficient to cover any outstanding cheques.

8. Conclusion

In conclusion, cheque bounce intimation failure can lead to serious legal and financial consequences for the issuer. It is important to respond promptly to any intimation regarding a cheque bounce, verify the contact information with the bank, and explore legal options if necessary. By providing accurate and up-to-date contact information to the bank and ensuring sufficient funds are available in the account, one can avoid cheque bounce intimation failure and maintain a good business relationship with the payee.

FAQs

What is a cheque bounce intimation?

A cheque bounce intimation is a notification sent by the bank to the issuer of the cheque when the cheque is bounced or returned unpaid due to insufficient funds, signature mismatch, or other reasons.

What happens if I don’t receive a cheque bounce intimation?

If you don’t receive a cheque bounce intimation, you may not be aware of the bounced cheque and may continue to use the account, which can result in further penalties and legal consequences.

What can cause a cheque bounce intimation failure?

Cheque bounce intimation failure can occur due to various reasons such as outdated contact information, connectivity issues, technical glitches, or errors in the bank’s system.

What should I do if I don’t receive a cheque bounce intimation?

If you don’t receive a cheque bounce intimation, you should contact the payee or the bank to verify the status of the intimation and take corrective action to update your contact information with the bank to avoid missing any future intimation.

What happens if a cheque is returned due to connectivity failure?

If a cheque is returned due to connectivity failure, the bank may retry the transaction or notify the issuer of the cheque bounce through alternative communication channels such as email or phone.

Try our Debt Resolution solutions today Request a Demo