Banking Challenges Unique to India

Embark on the journey of understanding the unique challenges faced by the banking sector in India. From non-performing assets to technological issues, discover the pivotal factors influencing the industry’s dynamics and strategies employed to overcome these hurdles.

Key Takeaways:

- Explore challenges like NPAs, technology issues, and political interference.

- Understand the impact on corporate governance and financial stability.

- Learn about proactive measures, including advancements in technology and regulatory reforms.

Navigating Banking Challenges in India:

In a dynamic financial landscape, India’s banking sector encounters multifaceted challenges. A notable concern is the surge in non-performing assets (NPAs), hindering credit and deposit growth. The Finance Committee’s report emphasizes the need for resolutions, suggesting a cautious approach toward public sector bank privatization.

Navigating Banking Challenges in India: In a dynamic financial landscape, India’s banking sector encounters multifaceted challenges. A notable concern is the surge in non-performing assets (NPAs), hindering credit and deposit growth. The Finance Committee’s report emphasizes the need for resolutions, suggesting a cautious approach toward public sector bank privatization.

A Bank is a financial institution that offers a wide range of services, including deposit accounts, lending, and investment products. Banks use the money deposits of one customer to provide loans and other financial services to other customers.

Banks play a vital role in the economy of every country as whole economic growth depends on it. They are the backbone of any economy; therefore, they must remain financially healthy.

However, with all of the increased responsibility, there are various banking challenges that have to come across. In this article, we will discuss the challenges a banking company faces and the measures they come across to curb these challenges.

In a report published by the finance committee, various issues and banking challenges are addressed. According to the report, the credit and deposit growth of banks has recently slowed down.

As the reason suggests, it is due to an increase in the volume of non-performing assets (NPAs), which restricts their ability to lend further. The challenges and recommendations as per the committee include:

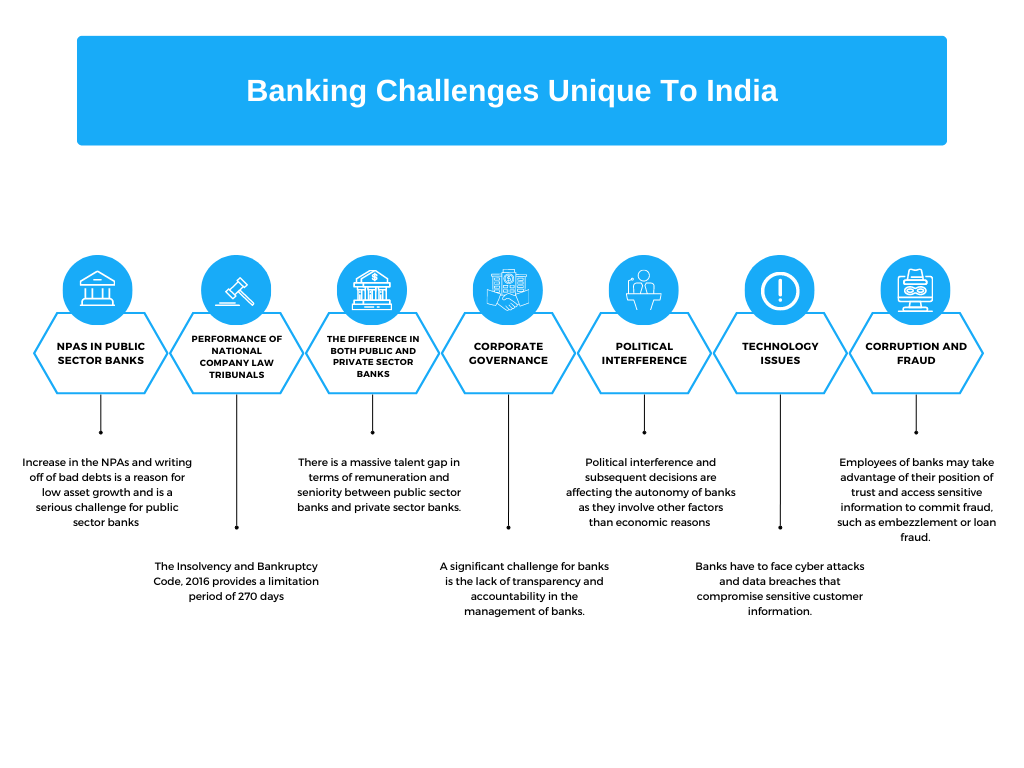

1. NPAs in public sector banks:

An NPA (Non-performing asset) is defined as a loan asset that has ceased to generate any income for a bank, whether in the form of interest or principal repayment. It has been observed that the increase in the NPAs and writing off of bad debts is a reason for low asset growth. This problem is more severe for public sector banks (PSBs) than private sector banks. However, it becomes better once the issue gets resolved through a legal mechanism such as the insolvency and bankruptcy code, 2016. It is recommended that to curb this banking challenge, there should not be more privatization of public sector banks.

2. Performance of National Company Law Tribunals (NCLT):

Another banking challenge is related to the performance of NCLT. The Insolvency and Bankruptcy Code, 2016 provides a limitation period of 270 days to dispose of any matter in Infront of NCLT. However, the dispute takes much longer than the time frame to dispose of. To overcome this challenge, it is a recommendation from the committee to increase the resources of NCLT that will help them to resolve the matter in the given time frame. Moreover, it is also a problem that lenders have to take large “haircuts.” The haircut is a term in the banking sector that refers to a lower-than-market-value price on an asset used as collateral for a loan. It is recommended by the community that IBC has to fix a reasonable price for haircuts to avoid loss for lenders.

3. The difference between both public and private sector banks:

There is a massive gap in the remuneration amount of senior management of public and private sector banks. Senior management is getting a much higher amount at private-sector banks than in the public sector. It is advisable to provide an equal incentive to the old authority of public banks. Similarly, CEOs in both banks also have a retirement age gap. In private sector banks, it is 70 years; however, in public sector banks is less. The retirement age should be increased in public banks similar to that of the private sector so that the expertise of senior authorities can be utilized properly.

4. Corporate Governance:

Corporate governance for banks refers to the system of rules, practices, and processes by which a bank is directed and controlled. A significant challenge for banks is the lack of transparency and accountability in the management of banks.

Banks are owned by large business groups, which leads to conflicts of interest and a lack of transparency in decision-making. There are also weak internal controls and compliance systems, which leads to mismanagement and fraud.

Banks are required to keep a certain number of independent boards of directors, but these directors are not genuinely independent. They have ties to the bank’s major shareholders and management.

This can make it difficult for the boards to effectively oversee management and ensure that the bank operates in the best interest of all stakeholders. Banks are taking necessary steps to take control over corporate governance, such as strengthening board composition and independence, enhancing risk management, enhancing shareholder engagement, and promoting ethical behavior.

5. Political Interference:

Political interference is another significant challenge for the banking sector. Decisions affect banks’ autonomy as they are taken more based on political rather than economic reasons. Political interference can favor specific individuals or companies over others, which can select the poor allocation of resources and impact on negative growth of the economy. Sometimes, it creates a lack of transparency in some transactions, making it challenging to address the issue of corruption. This influence leads to decisions that are not in the economy’s best interest. To curb this challenge, it is essential to have strong and independent regulatory bodies and laws limiting political interference in the banking sector. Additionally, regular audits and investigations should increase transparency to help reduce corruption and mismanagement.

6. Technology Issues:

Though the bank has obtained technology conveniently, these technologies are impacting its ability to operate effectively and efficiently. Banks have to face cyber attacks and data breaches that compromise sensitive customer information and lead to significant financial losses. They must also comply with many regulations, such as KYC, Anti-money laundering, and data privacy laws. Keeping up with these regulations can be a complex and expensive process. Banks are implementing multilayered security measures to curb the technology challenge and regularly monitoring their systems to prevent cyber-attacks. They are also investing in advanced security technologies like biometric authentication, artificial intelligence, and machine learning to improve the system’s security.

7. Corruption and fraud:

These are other banking challenges that are increasing each day. Employees of banks are taking advantage of their position of trust and accessing sensitive information to commit fraud, such as embezzlement or loan fraud. There is also an increase in several cases of money laundering. Bank employees accept a bribe to overlook the risk of money laundering activities. Banks are implementing various measures to curb these challenges, such as strengthening their internal controls and compliance procedure by conducting regular audits and investigations. Banks are also investing in new technologies like blockchain to improve transparency.

Conclusion:

Banking challenges are increasing day by day, which is lowering the account of profitability. Banks are facing various changes, such as technological advancement, suitable for cost-cutting, speedy transactions, and effective management. Still, it also leads to complex problems such as cyber-attacks, low security, data breach, etc. Banking committees regularly consider the increase in the number of banking challenges and work on refining new legislations, rules, and regulations to curb the need. A bank is a pillar of any economy; therefore, it is a must to tackle the problems and smoothen the process.

FAQs

1. What are the challenges faced by Indian banking?

In a report by the Finance Committee, issues such as slowed credit and deposit growth due to increased non-performing assets are highlighted, restricting further lending.

2. Why is banking challenging?

Banking deals with the masses, operating in a heavily regulated environment. Market size, operational complexities, and adherence to regulations make it inherently challenging.

3. What is the biggest threat to banks?

While cybersecurity remains a concern, credit risk in India poses a significant threat to banks striving for a positive bottom line.

Try our Debt Resolution solutions today Request a Demo