Allowing debt relief – a guide for Lenders

Debt relief for lenders is a crucial consideration for those who want to assist their clients in managing their financial obligations. In today’s uncertain economic climate, borrowers can quickly find themselves unable to repay their debts. This can be due to a variety of factors, including job loss, medical bills, or unexpected expenses.

To ensure that both parties are satisfied and that the borrower can get back on their feet, lenders must understand the process of granting debt relief. In this article, we will provide a comprehensive guide for lenders. The guide will focus on how to allow debt relief while still protecting their financial interests.

We will explore various forms of debt relief for lenders. We will discuss the benefits and drawbacks of each option and provide guidance on how to determine which type of debt relief is appropriate for different situations. By the end of this guide, lenders will have a better understanding of how to navigate the debt relief process and help their clients achieve financial stability.

When to Consider Debt Relief

As a lender, it is essential to identify when a borrower may be struggling financially and may require debt relief. Here are some early signs of financial distress to watch out for:

Early signs of financial distress

Late payments: When borrowers begin to miss payments or make them later than usual, it may indicate financial difficulties.

Increased credit utilization: Borrowers may begin to use their credit cards more often as a way to supplement their income, which can lead to a high credit utilization rate.

Decreased credit score: Financial distress can cause a drop in credit scores, which may indicate missed payments or high credit utilization.

Types of debt

Unsecured debt: Debt that is not backed by collateral, such as credit card debt, personal loans, or medical bills.

Secured debt: Debt that is backed by collateral, such as a mortgage or car loan.

Subprime debt: Debt that is given to borrowers with a high risk of default due to a low credit score or other financial issues.

Debt-to-income ratio

Lenders should also consider a borrower’s debt-to-income ratio (DTI), which is the amount of debt a borrower has compared to their income. A high DTI may indicate that a borrower is struggling to make ends meet and may require debt relief.

Severity of financial hardship

Finally, lenders should consider the severity of a borrower’s financial hardship. If a borrower has experienced a temporary setback, such as a job loss or medical emergency, debt relief for lenders may be a viable option. However, if a borrower’s financial situation is severe and unlikely to improve, debt relief may not be the best solution.

Debt Relief Options

When a borrower is struggling with debt, there are several debt relief options available to help them manage their financial obligations. Here are some debt relief options that lenders should be aware of:

Debt consolidation

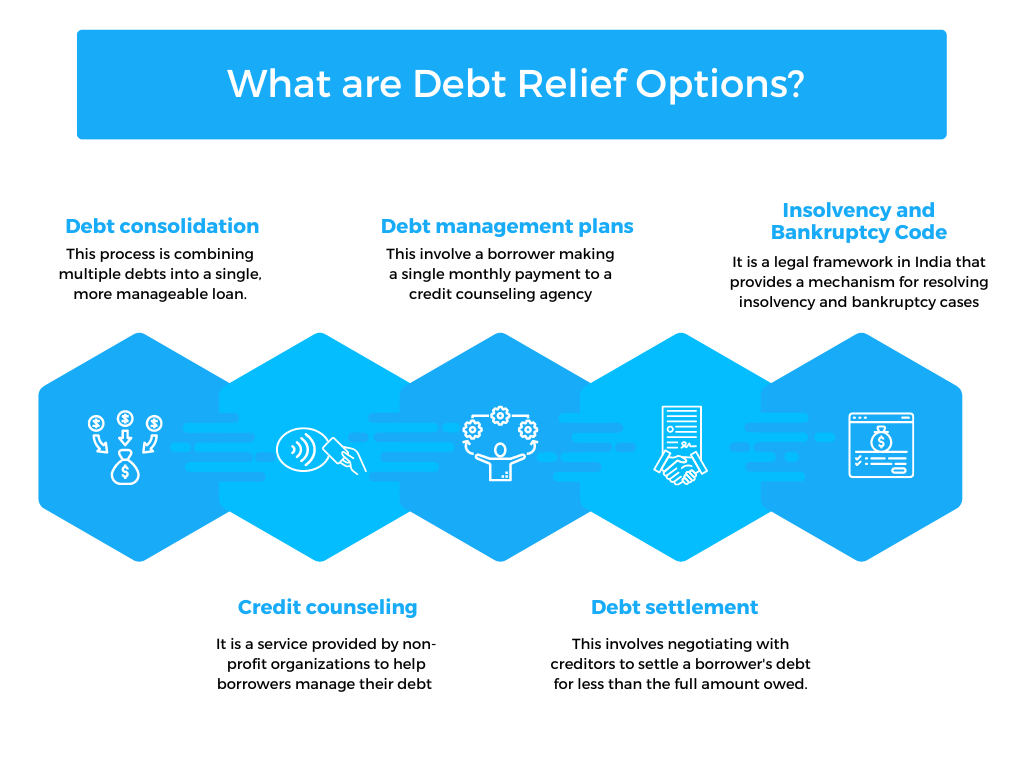

Debt consolidation is the process of combining multiple debts into a single, more manageable loan.

Types of debt consolidation: There are two main types of debt consolidation – secured and unsecured. Secured debt consolidation involves using collateral, such as a home or car, to secure the loan. Unsecured debt consolidation does not require collateral and is typically offered at a higher interest rate.

Pros and cons of debt consolidation: Debt consolidation can simplify a borrower’s repayment process, reduce their interest rates, and potentially lower their monthly payments. However, it may also result in a longer repayment period and a higher total cost of borrowing.

How debt consolidation can help lenders: Debt consolidation can help lenders reduce their risk of default by reducing the number of loans a borrower has and potentially lowering their interest rates.

Credit counseling

Credit counseling is a service provided by non-profit organizations to help borrowers manage their debt and develop a budget.

Services provided by credit counseling agencies: Credit counseling agencies provide financial education, debt management plans, and budgeting assistance to borrowers.

Pros and cons of credit counseling: Credit counseling can provide borrowers with valuable financial education and guidance. However, it may not be suitable for all borrowers, and some may require more intensive debt relief options.

How credit counseling can help lenders: Credit counseling can help lenders reduce their risk of default. This is done by providing borrowers with financial education and assistance in managing their debt.

Debt management plans

Explanation of debt management plans: Debt management plans involve a borrower making a single monthly payment to a credit counseling agency, which distributes the funds to their creditors.

How debt management plans work: Credit counseling agencies negotiate with creditors to reduce interest rates, waive fees, and develop a repayment plan.

Pros and cons of debt management plans: Debt management plans can simplify a borrower’s repayment process, reduce their interest rates and fees, and potentially lower their monthly payments. However, they may require a longer repayment period, and not all creditors may be willing to participate.

How debt management plans can help lenders: Debt management plans can help lenders reduce their risk of default by providing borrowers with a manageable repayment plan and reducing their interest rates and fees.

Debt settlement

Explanation of debt settlement: Debt settlement involves negotiating with creditors to settle a borrower’s debt for less than the full amount owed.

How debt settlement works: Borrowers typically work with a debt settlement company to negotiate with their creditors to settle their debt for a lump sum payment.

Pros and cons of debt settlement: Debt settlement can reduce a borrower’s total debt owed and potentially result in lower monthly payments. However, it may negatively impact a borrower’s credit score, and there is no guarantee that all creditors will agree to a settlement.

How debt settlement can help lenders: Debt settlement can help lenders reduce their risk of default by providing borrowers with a manageable repayment plan and potentially reducing the borrower’s total debt owed.

Insolvency and Bankruptcy Code (IBC)

The Insolvency and Bankruptcy Code is a legal framework in India that provides a mechanism for resolving insolvency and bankruptcy cases.

Types of IBC: There are two types of IBC – corporate insolvency and personal insolvency.

Pros and cons of IBC: IBC provides a legal framework for resolving insolvency and bankruptcy cases and can result in a more efficient resolution process. However, it may negatively impact a borrower

Factors to Consider When Offering Debt Relief

While debt relief for lenders options can be beneficial for borrowers, lenders need to consider several factors before offering debt relief. Here are some factors to consider when offering debt relief:

Risk assessment

Likelihood of repayment: Lenders need to assess the borrower’s ability to repay the debt before offering debt relief. This includes reviewing the borrower’s financial situation, income, and expenses.

Potential loss of revenue: Debt relief options may result in a loss of revenue for lenders. Lenders need to weigh the potential loss of revenue against the risk of default and decide if offering debt relief is a viable option.

Impact on credit risk: Debt relief for lenders options can have an impact on the borrower’s credit score and credit risk. Lenders need to consider the potential impact on their own credit risk when offering debt relief.

Compliance with regulations

Reserve Bank of India (RBI) guidelines: Lenders need to comply with RBI guidelines when offering debt relief. The RBI has issued guidelines on debt restructuring, which lenders need to follow.

Debt Recovery Tribunal (DRT) rules: Lenders need to comply with DRT rules when offering debt relief. DRT is a quasi-judicial body that deals with debt recovery cases.

Consumer Protection Act (CPA) regulations: Lenders need to comply with CPA regulations when offering debt relief. The CPA provides protection to consumers and regulates the rights of consumers in India.

Ethical considerations

Duty to treat customers fairly: Lenders have a duty to treat customers fairly when offering debt relief. This includes providing clear and transparent information to borrowers and treating them with respect and dignity.

Importance of maintaining customer relationships: Debt relief options can impact the relationship between lenders and borrowers. Lenders need to consider the importance of maintaining customer relationships and the potential impact on their reputation.

Conclusion

In conclusion, debt relief options can be helpful for borrowers who are facing financial difficulties. Lenders need to consider various factors when offering debt relief, including risk assessment, compliance with regulations, and ethical considerations.

To recap, lenders should consider debt relief when borrowers show early signs of financial distress, have unmanageable debt, high debt-to-income ratios, and are experiencing severe financial hardship. It is essential for lenders to prioritize borrower well-being and offer debt relief options when appropriate. By offering debt relief options, lenders can help borrowers manage their debt and avoid default, which can be beneficial for both borrowers and lenders.

In this regard, lenders should make an effort to educate borrowers on the various debt relief options available to them. Additionally, they should provide clear and transparent information about the potential benefits and drawbacks of each option.