What is DPD meaning in banking?

Days Past Due(DPD) refers to the number of days that a borrower has missed making a scheduled payment on a loan or credit account. DPD is used by banks and other lenders to track the payment history of their borrowers and to assess their creditworthiness.

The higher the DPD, the more risky the borrower is considered to be. In some cases, banks may use DPD to decide whether to grant a loan or extend credit to a borrower or to take action such as charging late fees, imposing penalties or initiating legal proceedings against the borrower.

For example, if a borrower was supposed to make a payment on their loan on the 15th of the month but missed it, and today is the 30th of the month, then the DPD for that payment would be 15 days.

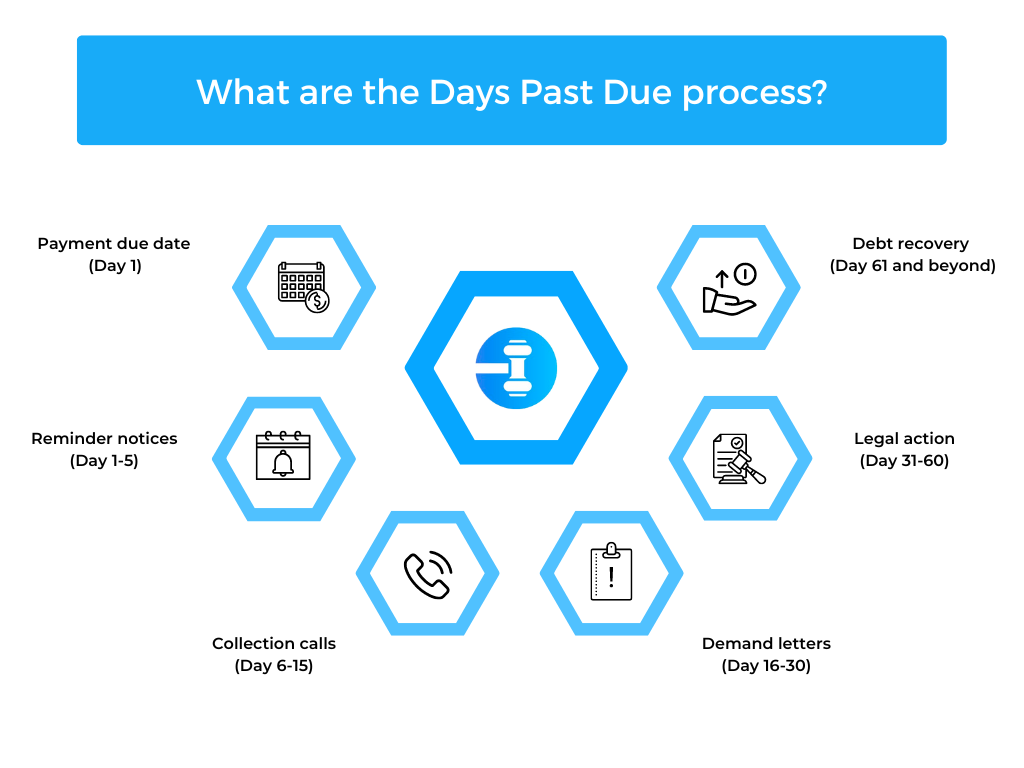

Days Past Due Process

The Days Past Due (DPD) is a process of series of steps that a bank or lender follows to manage the overdue payments of their borrowers. The exact steps of the DPD process may vary depending on the lender’s policies and the type of loan or credit account, but typically include the following:

- Payment due date: (Day 1) On the due date of the payment, the borrower is expected to make the payment in full. If the borrower misses the payment, the DPD count begins.

- Reminder notices: (Day 1-5) After the payment due date, the lender may send reminder notices to the borrower to inform them of the overdue payment and request immediate payment. These notices may be sent through email, text message, or phone call.

- Collection calls: (Day 6-15) If the borrower has not responded to the reminder notices, the lender may start making collection calls to the borrower. The calls may be made by an internal collections team or an external collections agency hired by the lender.

- Demand letters: (Day 16-30) If the borrower still does not respond or make the payment, the lender may send a demand letter to the borrower. The demand letter typically includes a warning of further actions the lender may take if the payment is not made, such as imposing late fees, reporting the delinquency to credit bureaus, or initiating legal action.

- Legal action: (Day 31-60) If the borrower still does not respond or make the payment, the lender may initiate legal action against the borrower, such as filing a lawsuit or placing a lien on the borrower’s assets.

- Debt recovery: (Day 61 and beyond) If the legal action is successful, the lender may recover the overdue amount through wage garnishment, bank account seizure, or asset liquidation. If the legal action is unsuccessful, the lender may write off the debt as a loss.

How long it takes to update CIBIL after paying all debts

After you have paid off all your debts, it may take some time for your CIBIL credit report to reflect the updated status. Generally, it takes around 30 to 45 days for the credit report to get updated with the new information.

This is because lenders and financial institutions typically report your repayment behavior to credit bureaus such as CIBIL at the end of each billing cycle, which could be monthly, quarterly, or semi-annually.

So, if you have paid off all your debts before the end of the billing cycle, it may take a little longer for the update to reflect on your credit report. Once the updated information is reported to CIBIL, it will reflect on your credit report within a few weeks.

You can check your CIBIL score and credit report after the due time to confirm that the information has been updated.

How are Days past due calculated?

To calculate Days Past Due (DPD), you need to first determine the due date of the payment. The calculation of DPD can vary depending on the organization or industry, but generally follows the same basic principles. This is typically the date on which the payment was originally scheduled to be made. Once you have the due date, you can compare it to the date on which the payment was actually made. If the payment was made on or before the due date, then the DPD is zero. If the payment was made after the due date, then the DPD is equal to the number of days between the due date and the date on which the payment was made.

For example, if the due date for a payment was January 1st and the payment was made on January 15th, then the DPD would be 14 (since the payment was 14 days late).

How do you calculate overdue invoice days?

To calculate overdue invoice days, you need to know the due date of the invoice and the current date. You can then subtract the due date from the current date to get the number of days overdue.

For example, if an invoice was due on March 15, 2023, and today is March 29, 2023, the invoice is 14 days overdue. You can calculate this by subtracting the due date (March 15) from the current date (March 29): 14 = 29 – 15. So, the overdue invoice days in this case would be 14 days.

How Can I remove DPD from CIBIL

What is DPD in credit risk?

DPD (Days Past Due) is a commonly used metric in credit risk management to indicate the number of days that a payment on an account or loan is overdue. It is a measure of how many days a customer has failed to make a payment beyond the due date.

For example, if a customer has a loan or credit account with a monthly payment due date on the 15th of every month, and they fail to make the payment until the 20th of the same month, the DPD for that payment would be 5 days.

DPD is an important metric in credit risk because it can be used to identify customers who may be experiencing financial difficulties or are at risk of defaulting on their payments. By tracking DPD over time, lenders and creditors can also monitor the creditworthiness of their customers and take appropriate measures to manage credit risk.

Recover CIBIL score

If you have a low CIBIL score and want to improve it, here are some steps you can take:

- Review your credit report: Get a copy of your credit report from CIBIL and review it for any errors or discrepancies. Dispute any inaccuracies with CIBIL.

- Pay off outstanding debts: Make sure you pay off any outstanding debts, such as credit card balances, as soon as possible. This can help improve your credit utilization ratio, which is an important factor in your CIBIL score.

- Avoid late payments: Make sure you pay all your bills on time. Late payments can have a significant negative impact on your CIBIL score.

- Maintain a good credit mix: Having a mix of different types of credit, such as credit cards, loans, and mortgages, can help improve your credit score.

- Avoid multiple credit applications: Avoid applying for multiple loans or credit cards at the same time. Each application results in a hard inquiry on your credit report, which can lower your score.

- Use credit responsibly: Use your credit card responsibly and avoid maxing out your credit limit.

What Does 30 days due mean?

Calculate DPD days

To calculate DPD (Days Past Due) days, you need to know the due date of the payment and the date on which it was actually paid.

For example, if a payment was due on March 15, 2023, but it was paid on March 29, 2023, the DPD would be 14 days, since the payment was made 14 days after the due date.

You can calculate the DPD by subtracting the due date from the date on which the payment was actually made.

DPD = Date of Payment – Due Date

In this example, the calculation would be:

DPD = March 29, 2023 – March 15, 2023

DPD = 14 days

Therefore, the DPD days for this payment would be 14 days.

Does past due affect credit score

Yes, past-due payments can have a negative impact on your credit score. When you have a past due payment, it means you’ve missed the payment due date by some number of days. This information is typically reported to credit bureaus and reflected on your credit report, where it can remain for up to seven years. Late payments are one of the most significant factors that can affect your credit score. Payment history makes up 35% of your FICO credit score, which is a widely used credit scoring model. The more late payments you make, the more negative impact it will have on your credit score.

The impact of a past due payment on your credit score depends on several factors, including how late the payment is, the number of past due payments, the amount of the payment, and how recently the late payment occurred. A single late payment can lower your credit score by several points, while multiple late payments can have a much more significant impact on your credit score.

To maintain a good credit score, it is essential to make all your payments on time and avoid past due payments. If you do have a past due payment, it’s important to pay it as soon as possible to minimize the negative impact on your credit score.

Is past due the same as Overdue

In the context of credit payments, “past due” and “overdue” are often used interchangeably and refer to a payment that has not been made by its due date. However, there can be slight differences in their meaning depending on the context. “Past due” typically refers to a payment that is not made by the due date, but may not necessarily have incurred any additional fees or penalties. For example, if a payment is due on the 15th of the month, and it is not made until the 20th of the same month, the payment is considered past due.

“Overdue” generally refers to a payment that is not made by the due date and has also incurred additional fees or penalties as a result. For example, if a payment is due on the 15th of the month, and it is not made until the 25th of the same month, the payment is considered overdue and may incur late payment fees or interest charges. In practice, the terms past due and overdue are often used interchangeably, and both indicate that a payment has not been made by the due date.

What is the overdue penalty?

The overdue penalty is a fee charged for not returning borrowed items or paying bills by their due date. It is typically imposed as a percentage of the amount owed, and the exact penalty amount can vary depending on the organization or institution that has issued the loan or bill. Overdue penalties are intended to encourage people to return borrowed items on time and to discourage late payments, as they can be costly and add up quickly if left unpaid.

Conclusion

In conclusion, due past days in a credit report is a crucial factor that lenders and creditors consider when determining an individual’s creditworthiness. It represents the number of days that a borrower has failed to make payments on their credit accounts. A high number of due past days can negatively impact an individual’s credit score and make it difficult for them to secure loans or credit in the future. It is important for individuals to regularly monitor their credit reports and ensure that their payment history is accurate and up-to-date. Making timely payments and keeping due past days to a minimum can help improve one’s credit score and increase their chances of being approved for credit in the future.