The Rise of NBFCs in India: A Catalyst for Financial Growth

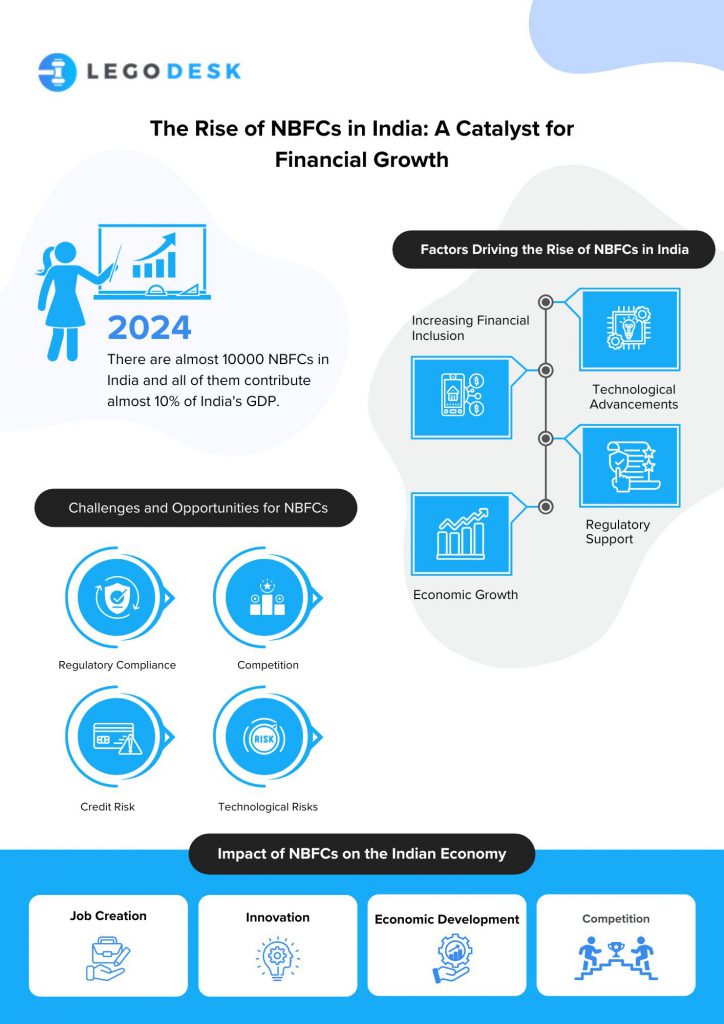

Non-Banking Financial Companies (NBFCs) have emerged as pivotal players in the Indian financial landscape, driving growth and innovation. As of 2023, there are almost 10000 NBFCs in India and all of them contribute almost 10% of India’s GDP. Their role in providing a diverse range of financial services, from lending and insurance to asset management, has been instrumental in meeting the evolving needs of individuals and businesses. This essay delves into the factors contributing to the rise of NBFCs in India, their impact on the economy, and the challenges and opportunities they face in the future.

Factors Driving the Rise of NBFCs in India

Several key factors have fueled the rapid expansion of NBFCs in India:

- Increasing Financial Inclusion: NBFCs have played a crucial role in promoting financial inclusion by reaching underserved segments of the population, including rural areas, micro, small, and medium enterprises (MSMEs), and women entrepreneurs. Their ability to offer tailored financial products and services has enabled these segments to participate more actively in the economy.

- Technological Advancements: The rise of NBFCs in India can be attributed to the advent of digital technologies. Leveraging artificial intelligence, machine learning, and big data analytics, NBFCs can now offer faster, more efficient, and personalized financial solutions. This has lowered barriers to entry for both consumers and businesses, driving growth in the sector.

- Regulatory Support: The Reserve Bank of India (RBI) has implemented favorable policies and regulations to support the growth of NBFCs. This includes measures such as easing licensing requirements, improving access to funding, and enhancing oversight to ensure financial stability.

- Economic Growth: India’s robust economic growth has created a favorable environment for NBFCs to thrive. As businesses expand and consumer spending increases, the demand for financial services has surged, providing ample opportunities for NBFCs to capitalize on.

Impact of NBFCs on the Indian Economy

The growth of NBFCs has had a significant impact on the Indian economy. Some key benefits include:

- Job Creation: NBFCs have created numerous jobs, both directly and indirectly, contributing to employment generation and reducing unemployment rates.

- Economic Development: By providing financial support to MSMEs and other businesses, NBFCs have played a vital role in driving economic development, particularly in rural areas.

- Innovation: NBFCs have been at the forefront of financial innovation, introducing new products and services that meet the evolving needs of customers. This has helped to improve financial efficiency and accessibility.

- Competition: The presence of NBFCs has increased competition in the financial services sector, leading to better terms, lower interest rates, and improved customer service.

Challenges and Opportunities for NBFCs

Despite their impressive growth, NBFCs face several challenges and opportunities:

- Regulatory Compliance: Adhering to increasingly complex regulatory requirements can be burdensome for NBFCs. Ensuring compliance with regulations related to capital adequacy, risk management, and consumer protection is essential for their long-term sustainability.

- Competition: Competition from banks, fintech startups, and other financial institutions is intensifying. NBFCs must differentiate themselves by offering unique value propositions and leveraging their strengths in niche areas.

- Credit Risk: Managing credit risk is a critical challenge for NBFCs. The ability to assess borrower creditworthiness accurately is essential to prevent defaults and maintain profitability.

- Technological Risks: The increasing reliance on technology exposes NBFCs to cyber security threats and operational risks. Investing in robust IT infrastructure and security measures is crucial to protect their operations and customer data.

Opportunities for Growth

Despite the challenges, the rise of NBFCs in India is going to be unstoppable.

- Digital Transformation: Continued investment in digital technologies can help NBFCs improve efficiency, reduce costs, and enhance customer experience.

- Niche Markets: Focusing on niche market segments can provide NBFCs with a competitive advantage. By specializing in specific areas, such as microfinance, housing finance, or asset management, NBFCs can build expertise and cater to the unique needs of their target customers.

- Strategic Partnerships: Collaborating with other financial institutions, technology providers, and government agencies can create new opportunities for NBFCs to expand their reach and offer innovative products and services.

- International Expansion: As India’s economic influence grows, NBFCs have the potential to expand their operations into international markets. This can provide new sources of revenue and diversification.

Conclusion

The growth of NBFCs in India has been a remarkable success story. Their contributions to financial inclusion, economic development, and innovation have been significant. As the sector continues to evolve, NBFCs must navigate the challenges and seize the opportunities to maintain their momentum and play a vital role in shaping the future of Indian finance. By focusing on digital transformation, niche market specialization, strategic partnerships, and international expansion, NBFCs can position themselves for sustainable growth and continued success.

FAQs

1. What are the key factors driving the growth of NBFCs in India?

Several factors have contributed to the remarkable growth of NBFCs in India. Firstly, NBFCs have played a pivotal role in promoting financial inclusion by reaching underserved segments of the population, such as rural areas, micro, small, and medium enterprises (MSMEs), and women entrepreneurs. This has enabled these segments to participate more actively in the economy. Secondly, technological advancements have transformed the way NBFCs operate. Leveraging artificial intelligence, machine learning, and big data analytics, NBFCs can now offer faster, more efficient, and personalized financial solutions. This has lowered barriers to entry for both consumers and businesses, driving growth in the sector. Thirdly, the Reserve Bank of India (RBI) has implemented favorable policies and regulations to support the growth of NBFCs. This includes measures such as easing licensing requirements, improving access to funding, and enhancing oversight to ensure financial stability. Finally, India’s robust economic growth has created a favorable environment for NBFCs to thrive. As businesses expand and consumer spending increases, the demand for financial services has surged, providing ample opportunities for NBFCs to capitalize on.

2. What are the main benefits of NBFCs to the Indian economy?

The growth of NBFCs has had a significant impact on the Indian economy. They have created numerous jobs, both directly and indirectly, contributing to employment generation and reducing unemployment rates. By providing financial support to MSMEs and other businesses, NBFCs have played a vital role in driving economic development, particularly in rural areas. Additionally, NBFCs have been at the forefront of financial innovation, introducing new products and services that meet the evolving needs of customers. This has helped to improve financial efficiency and accessibility. Moreover, the presence of NBFCs has increased competition in the financial services sector, leading to better terms, lower interest rates, and improved customer service.

3. What are the challenges faced by NBFCs in India?

Despite their impressive growth, NBFCs face several challenges. Adhering to increasingly complex regulatory requirements can be burdensome for NBFCs. Ensuring compliance with regulations related to capital adequacy, risk management, and consumer protection is essential for their long-term sustainability. Competition from banks, fintech startups, and other financial institutions is intensifying, requiring NBFCs to differentiate themselves by offering unique value propositions and leveraging their strengths in niche areas. Managing credit risk is another critical challenge for NBFCs. The ability to assess borrower creditworthiness accurately is essential to prevent defaults and maintain profitability. Furthermore, the increasing reliance on technology exposes NBFCs to cyber security threats and operational risks. Investing in robust IT infrastructure and security measures is crucial to protect their operations and customer data.

4. What opportunities do NBFCs have for future growth?

Despite the challenges, NBFCs have several opportunities for growth. Continued investment in digital technologies can help NBFCs improve efficiency, reduce costs, and enhance customer experience. Focusing on niche market segments can provide NBFCs with a competitive advantage. Collaborating with other financial institutions, technology providers, and government agencies can create new opportunities for NBFCs to expand their reach and offer innovative products and services. Additionally, as India’s economic influence grows, NBFCs have the potential to expand their operations into international markets.

5. How can NBFCs contribute to the sustainable development of India?

NBFCs can contribute to the sustainable development of India in several ways. By reaching underserved segments of the population, they can help reduce poverty and inequality. NBFCs can play a crucial role in providing financial support to MSMEs, which are vital for job creation and economic growth. Additionally, NBFCs can drive innovation in the financial services sector, leading to new products and services that benefit customers. By ensuring that borrowers can repay their loans, NBFCs can contribute to financial stability and prevent debt traps. In conclusion, NBFCs have the potential to play a significant role in India’s sustainable development by promoting financial inclusion, supporting MSMEs, driving innovation, and adhering to responsible lending practices.