Lok Adalat Success Rate in Loan Recovery: An Essential Tool in India’s Debt Resolution Landscape

Non-Performing Assets (NPAs) continue to challenge the Indian banking and financial sector, affecting banks’ profitability and overall financial stability. Efficient recovery of bad loans is crucial for maintaining the health of financial institutions and ensuring credit flow to productive segments of the economy. Among various mechanisms deployed for loan recovery, Lok Adalats have emerged as a vital, cost-effective, and speedy alternative for resolving smaller loan defaults, especially in the pre-litigation stage.

Lok Adalat, meaning “People’s Court,” is an alternative dispute resolution mechanism established under the Legal Services Authorities Act, 1987. It provides an informal, conciliatory platform where cases related to pending court disputes or pre-litigation matters can be amicably settled through mutual agreement without prolonged litigation. Lok Adalats can handle a wide array of disputes, including civil, matrimonial, and notably, loan recovery cases up to ₹20 lakh as per RBI guidelines.

The system is non-adversarial, encouraging negotiation and compromise, thus saving time and reducing legal expenses for both lenders and borrowers.

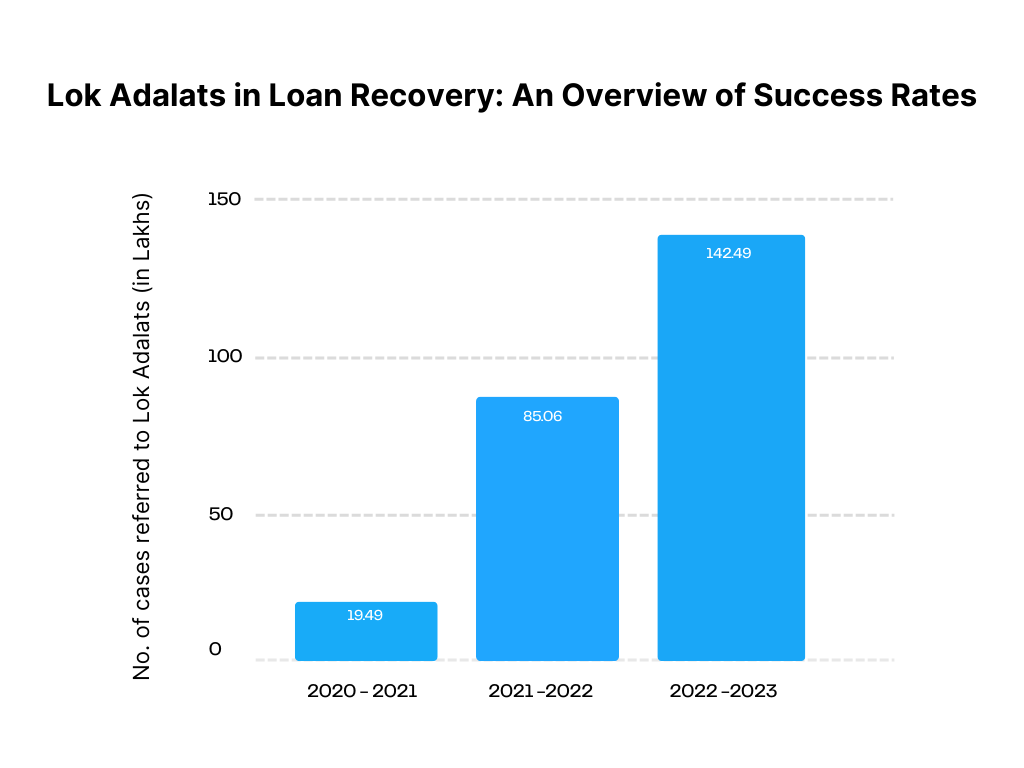

Lok Adalats in Loan Recovery: An Overview of Success Rates

Lok Adalats have become increasingly popular for settling small-ticket loan defaults that may not be viable for lengthy court proceedings or Debt Recovery Tribunals (DRTs). The approach is attractive due to its simplicity, speed, and low-cost settlement process.

– In the financial year 2022-23, over 14.2 million cases involving ₹1.88 lakh crore were referred to Lok Adalats for resolution.

– However, the actual recovery rate from these cases has remained moderate. For example, in 2021-22, the recovery stood at around ₹2,778 crore, which was approximately 2.3% of the total amount referred.

– This low recovery percentage reflects the inherent challenges of recovering small-value loans (small-ticket NPAs), where defaulters may lack the capacity or willingness to repay.

– Despite modest recovery percentages, Lok Adalats have demonstrated stable recovery incomes over the years, emphasizing their role in the loan recovery ecosystem alongside legal routes like DRTs and SARFAESI.

Comparative Effectiveness with Other Recovery Mechanisms

– Debt Recovery Tribunals (DRTs) tend to have higher recovery success rates, around 15-25%, because they deal with larger-ticket loans.

– The Insolvency and Bankruptcy Code (IBC) has shown recovery rates ranging between 30-50%, providing a more time-bound and structured insolvency resolution process.

– Lok Adalats, on the other hand, excel in quick resolution of a large volume of small cases with fewer procedural complexities, although the monetary recovery per case may be smaller.

Factors Contributing to Lok Adalat Success in Loan Recovery

– Volume Handling: Lok Adalats process a high volume of cases swiftly, which helps clear backlog and reduce the burden on formal courts.

– Pre-Litigation Focus: They provide an early platform for settlement before cases escalate to more complex litigation or tribunals.

– Cost-Effectiveness: Lower legal costs for both banks and borrowers encourage settlements.

– Mobile Lok Adalats: Innovative mobile Lok Adalats travel to different locations to resolve disputes promptly, improving accessibility and outreach.

– Collaborative Efforts: Coordination between banks and legal service authorities enhances the functioning and effectiveness of Lok Adalats.

Challenges and Limitations

– Recovery percentages are relatively low because small-value default cases often involve financially weak borrowers.

– The enforcement of Lok Adalat awards, while final and binding, can face practical hurdles without proper follow-ups.

– Lack of awareness among borrowers and banks about the benefits and procedures of Lok Adalat sometimes limits utilization.

Conclusion: Lok Adalats as a Valuable Loan Recovery Solution

Lok Adalats are a pivotal mechanism in India’s debt recovery framework—especially in addressing the large volume of small to medium ticket NPAs that traditional judicial processes might find inefficient to manage. Although the recovery rates by value may appear modest compared to other routes, the sheer scale and speed at which they operate make Lok Adalats indispensable to banks and financial institutions.

For lenders, Lok Adalats offer a frictionless, cost-effective avenue to recover loans and reduce non-performing assets. For borrowers, they provide a less adversarial, quicker means to resolve dues, often with mutually agreeable terms. Strengthening awareness, increasing frequency of Lok Adalat sessions, and improving enforcement can further boost their success in loan recoveries.

Legodesk remains committed to supporting modern legaltech solutions that integrate Lok Adalat processes, helping stakeholders navigate loan recovery with agility and efficiency.

FAQs

- What are Lok Adalats and how do they help in loan recovery?

Ans: Lok Adalats are alternative dispute resolution forums where loan recovery disputes are settled amicably and quickly without protracted litigation, making them efficient for small to medium loan defaults.

- What kinds of loan cases are eligible to be referred to Lok Adalats?

Ans: Typically, personal loans, credit card loans, housing loans, and other loans with outstanding amounts up to Rs 20 lakh are referred to Lok Adalats for settlement.

- How effective are Lok Adalats in recovering loan amounts?

Ans: While the recovery rate may be modest (around 2-3%), Lok Adalats handle a very high volume of cases efficiently, providing quick resolutions and reducing the burden on courts.

- What is the process of settling a loan case in a Lok Adalat?

Ans: A mediation session is conducted between the borrower and lender, facilitated by a panel including legal experts, where both parties negotiate and mutually agree on settlement terms, which are then legally binding.

- Are Lok Adalat awards legally enforceable?

Ans: Yes, the settlement reached in a Lok Adalat is binding on both parties and is treated as a decree of a civil court, enforceable by law.

- What are the advantages of using Lok Adalats for loan recovery?

Ans: They offer cost-effective, speedy resolution, reduce legal fees, ease court burdens, and provide an amicable environment encouraging cooperation between lenders and borrowers.

- What limitations or challenges are associated with Lok Adalats in loan recovery?

Ans: Challenges include low overall recovery rates by value, enforcement difficulties, limited borrower awareness, and a high proportion of financially weak defaulters, necessitating better follow-up mechanisms.