Mounting Debt: Know if it is time for MSME Loan Restructuring

India’s Micro, Small, and Medium Enterprises (MSMEs) are the vibrant engine of the nation’s economy. They are diverse, innovative, and contribute significantly to GDP, exports, and employment generation, providing livelihoods for crores of Indians. From small manufacturing units in Pune to handicraft businesses in Jaipur and IT service providers in Bengaluru, MSMEs operate across every sector, embodying the entrepreneurial spirit of the country.

However, this dynamic sector is not without its vulnerabilities. MSMEs often operate with limited capital, face intense competition, and are particularly susceptible to economic downturns, supply chain disruptions, and delays in payments from larger entities. Access to timely and affordable credit can be a persistent challenge, and managing debt effectively is crucial for their survival and growth. When faced with unexpected crises or prolonged periods of poor performance, MSMEs can find themselves in dire financial straits, struggling to meet their commitments.

In such challenging times, understanding the available options becomes paramount. Continuing without addressing mounting debt can lead to severe consequences, including the complete collapse of the business. For Indian MSMEs grappling with financial distress, two significant formal avenues exist: exploring MSME loan restructuring with lenders or, in more severe cases, considering a resolution process under the Insolvency and Bankruptcy Code (IBC), which can lead to bankruptcy or revival. Additionally, for specific types of loan disputes, Lok Adalat offers an alternative path for amicable settlement. This blog delves into these options, helping Indian MSMEs understand when and why they might consider each.

Early Warning Signs: Recognizing the Red Flags Before the Storm Hits

Proactive identification of financial distress is the first and most critical step. Many MSMEs delay acknowledging the problem, hoping for a tự nhiên turnaround. However, early intervention significantly increases the chances of successful resolution. Be vigilant for these warning signs:

- Consistent Decline in Sales and Profitability: A downward trend in revenue and shrinking profit margins over several quarters are clear indicators of trouble. This could be due to market factors, increased competition, or operational inefficiencies.

- Difficulty in Meeting Operational Expenses: Struggling to pay for raw materials, utilities, rent, or even salaries on time signals severe cash flow constraints.

- Increasing Reliance on Short-Term Debt: Using overdrafts or high-interest short-term loans to cover regular expenses or repay existing debt is a dangerous cycle that indicates a fundamental mismatch between income and expenditure.

- Delayed Payments to Suppliers and Creditors: Straining relationships with suppliers by delaying payments can disrupt your supply chain and lead to a loss of creditworthiness within the business ecosystem.

- Frequent Overdrawing in Bank Accounts: Regularly exceeding your sanctioned limits or facing bounced cheques is a strong indicator of poor liquidity management and impending financial crisis.

- Deterioration in Key Financial Ratios: Monitoring ratios like the current ratio (current assets divided by current liabilities), debt-to-equity ratio, and interest coverage ratio can provide objective insights into the financial health of your business. A declining current ratio, increasing debt-to-equity, or insufficient interest coverage are red flags.

- Adverse External or Internal Credit Ratings: A downgrade in your credit rating by agencies or a negative assessment by your bank signals increased risk and will make accessing future credit difficult and expensive.

- Loss of Key Customers or Market Share: Losing significant clients or seeing your market share erode directly impacts revenue and future viability.

- Mounting Inventory or Unsold Stock: If your finished goods are piling up, it indicates a problem with sales, production, or market demand, tying up crucial working capital.

- Chasing Receivables Aggressively: While managing receivables is normal, excessive time and effort spent on recovering payments might indicate issues with your credit policy or the financial health of your customers.

If your MSME is experiencing one or more of these signs, it’s time to take proactive steps. Ignoring these red flags can lead to a rapid deterioration of your financial situation, limiting your options for recovery.

MSME Loan Restructuring: A Negotiated Path to Recovery

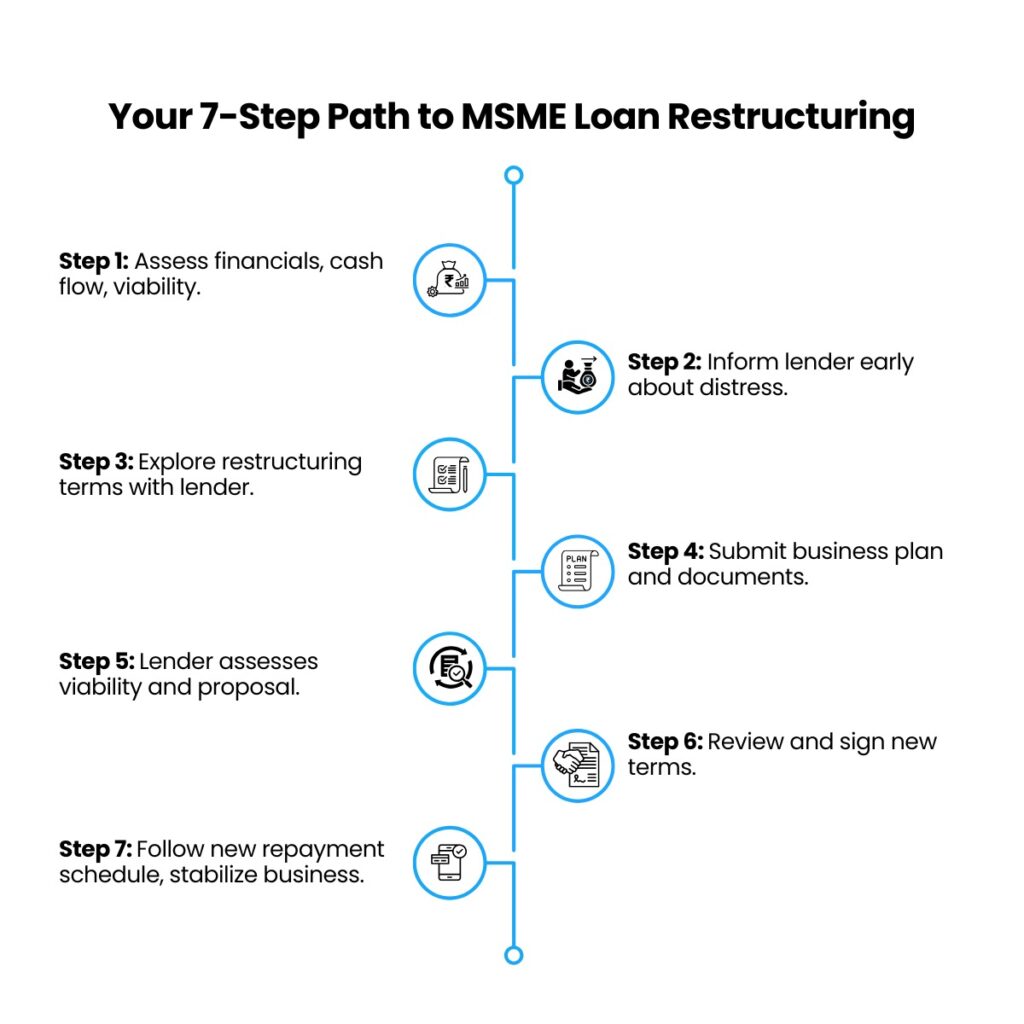

For many Indian MSMEs facing temporary financial headwinds but with a fundamentally viable business, MSME loan restructuring offers a powerful tool to regain financial stability. This process involves engaging with your lenders (banks or Non-Banking Financial Companies – NBFCs) to modify the original terms and conditions of your existing loan facilities. The goal is to create a revised repayment plan that aligns better with the current or projected cash flow of your business, making debt servicing more manageable.

MSME loan restructuring is often preferred when the financial distress is a result of external, temporary factors (like a specific industry downturn, impact of a pandemic, or a large client default) rather than inherent flaws in the business model. It’s an acknowledgment of difficulty but also a demonstration of intent to repay the debt under revised, more realistic terms.

Common Elements of MSME Loan Restructuring:

Lenders, often guided by RBI directives and their internal policies, may offer various concessions as part of an MSME loan restructuring package:

- Extension of Loan Tenure: Stretching the repayment period is a common approach to reduce the Equated Monthly Installment (EMI) amount, easing the monthly cash outflow burden.

- Changes in Interest Rate: In some cases, lenders might agree to a temporary reduction in the interest rate, although this is less common than tenure extension.

- Granting a Moratorium Period: A temporary pause or reduction in loan repayments (principal and/or interest) for a defined period can provide crucial breathing space for the MSME to stabilize its finances.

- Rescheduling of Payments: Adjusting the frequency or timing of payments to match seasonal business cycles.

- Conversion of Working Capital into Term Loan: Overdue working capital limits can sometimes be converted into a structured term loan repayable over a longer period.

- Waiver of Penal Interest or Charges: Lenders might consider waiving accumulated penal interest or other charges to reduce the total outstanding amount.

The process for MSME loan restructuring typically involves the MSME submitting a formal application to their lender, along with a detailed analysis of the reasons for financial distress and a projected business plan demonstrating how the business will become viable and service the restructured debt. The lender will then assess the proposal, the viability of the business, and the borrower’s willingness to cooperate before deciding on the restructuring terms.

Advantages of MSME Loan Restructuring:

- Continued Operations: The most significant benefit is avoiding immediate default, allowing the business to continue its activities and work towards recovery.

- Improved Cash Flow Management: Lower EMIs and/or a moratorium directly improve liquidity, enabling the MSME to cover essential operating costs and potentially invest in revival strategies.

- Prevention of NPA Classification: Successfully implementing a MSME loan restructuring plan can prevent the loan account from being classified as an NPA, preserving the MSME’s credit history to some extent.

- Opportunity for Revival: For a fundamentally sound business facing temporary issues, restructuring provides the necessary breathing room to overcome challenges and return to profitability.

- Maintaining Lender Relationship: Working collaboratively with your lender through restructuring can help maintain a positive relationship for future credit needs.

Potential Disadvantages of MSME Loan Restructuring:

- Impact on Credit Score: While less severe than default, a restructured loan is still reported to credit bureaus and can negatively impact the MSME’s credit score, making future borrowing potentially more difficult or expensive.

- Increased Total Interest: Extending the loan tenure, while reducing EMIs, will likely result in paying more interest over the life of the loan.

- Requires Lender Approval: Restructuring is not an automatic right; it depends on the lender’s assessment of the business’s viability and their willingness to restructure.

- Not a Guarantee of Success: Restructuring provides an opportunity, but the ultimate success depends on the MSME’s ability to execute its revised business plan and improve performance.

MSME loan restructuring is a powerful tool for eligible businesses, offering a chance to overcome temporary setbacks and continue their journey. It requires transparency, a credible plan, and active engagement with lenders.

Lok Adalat: An Alternative for Settling Loan Disputes Amicably

Beyond formal restructuring, Indian MSMEs facing loan repayment issues, particularly with accounts that may have already become irregular or classified as NPAs, can explore resolution through the mechanism of Lok Adalat. Established under the Legal Services Authorities Act, 1987, Lok Adalats serve as informal forums for amicable settlement of disputes, including various financial matters and loan recovery cases.

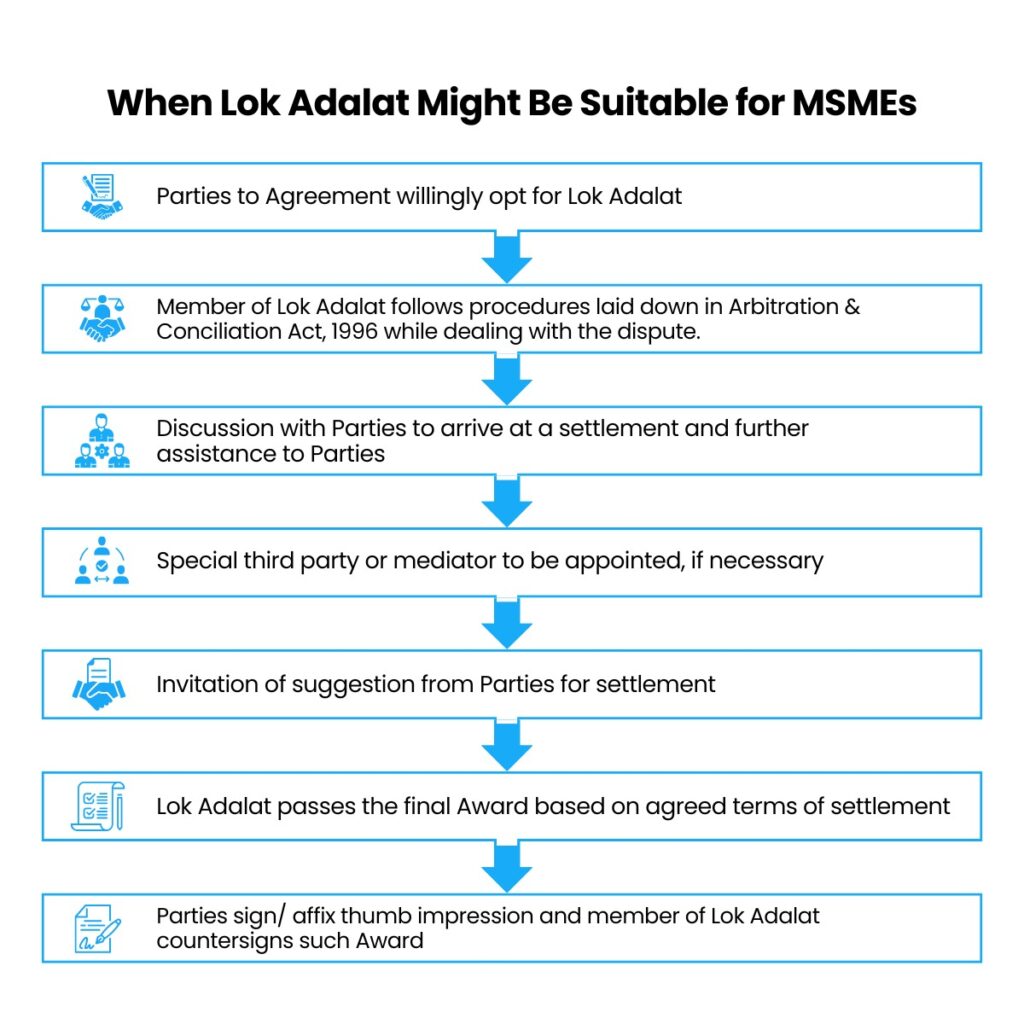

Lok Adalats are organized periodically by Legal Services Authorities at the national, state, and district levels. They bring together parties to a dispute – in this case, the MSME borrower and the lender – under the guidance of a panel typically comprising a judicial officer (sitting or retired), a lawyer, and a social worker. The panel acts as a conciliator, facilitating dialogue and negotiation to arrive at a mutually acceptable settlement.

How Lok Adalat Works for MSME Loan Cases:

When an MSME loan account is referred to a Lok Adalat (either by the bank, or sometimes at the borrower’s request, or when a case is pending in court), both parties are issued notices to appear. The panel hears both sides, understands the reasons for default, and explores possibilities for a compromise settlement. This settlement often involves a ‘One-Time Settlement’ (OTS) amount, which might be less than the total outstanding dues, including accumulated interest and charges.msme Lenders may agree to a reduced amount to ensure quicker recovery and avoid the costs and uncertainties of prolonged litigation or formal insolvency proceedings.

If a settlement is reached, it is documented as an ‘Award’ by the Lok Adalat. This award is legally binding on both parties and is deemed a decree of a civil court. No appeal lies against such an award in any court of law.

When Lok Adalat Might Be Suitable for MSMEs:

Lok Adalat is often a suitable option for MSMEs when:

- The loan amount is relatively small (though limits can vary and have been increased over time for bank NPAs).

- The loan account has already become an NPA, and formal MSME loan restructuring avenues for standard assets are not applicable.

- The MSME is willing to make a lump-sum payment or adhere to a short repayment schedule for a reduced settlement amount.

- Both the MSME and the lender are open to negotiating a compromise settlement to avoid lengthy legal battles.

- The case is pending in court or is at a pre-litigation stage where settlement is being explored.

Advantages of Resolving Through Lok Adalat:

- Amicable and Mutually Agreed Solution: The settlement is reached through negotiation, offering a less adversarial approach compared to litigation.

- Speedy Resolution: Cases in Lok Adalat are typically resolved much faster than in regular courts.

- Cost-Effective: No court fee is involved, making it an economical option for settlement.

- Binding and Executable Order: The Lok Adalat award is legally binding and can be executed as a court decree.

- Opportunity for Debt Closure: It provides a mechanism for the MSME to close a defaulted loan account, albeit with a “settled” status on the credit report.

Limitations of Lok Adalat:

- Compromise May Involve Waivers: While advantageous for the borrower, it means the lender takes a haircut on the outstanding amount.

- Impact on Credit Score: A loan settled through Lok Adalat will be reported as “settled” on the credit report, negatively impacting future creditworthiness for a significant period.

- Not Suitable for Complex Cases: Complex financial structures or disputes involving multiple lenders and intricate legal issues are less likely to be resolved effectively in Lok Adalat.

- Depends on Lender’s Policy: The extent of waiver or settlement offered by the lender will depend on their internal policies and assessment of the case.

Lok Adalat serves as a valuable alternative dispute resolution mechanism for MSMEs, offering a pathway to settle loan disputes, particularly those classified as NPAs, in a more accessible and time-bound manner than traditional courts.

Bankruptcy (IBC): The Last Resort for Resolution or Closure

When MSME loan restructuring is not feasible, successful, or sufficient to revive the business, and Lok Adalat is not applicable or effective, the formal insolvency and bankruptcy process under the Insolvency and Bankruptcy Code (IBC), 2016, becomes the avenue for resolution. IBC provides a comprehensive legal framework for the insolvency resolution or liquidation of corporate debtors, including MSMEs, in a time-bound manner.

The primary objective of the IBC is to maximize the value of assets of the corporate debtor, promote entrepreneurship, and balance the interests of all stakeholders.

The IBC Process (Briefly):

When an MSME defaults on a debt above a prescribed threshold (currently ₹1 crore for corporate debtors), a financial creditor, operational creditor, or the corporate debtor itself can initiate the Corporate Insolvency Resolution Process (CIRP) before the National Company Law Tribunal (NCLT). Under CIRP, the management is taken over by an Interim Resolution Professional (IRP), and a Committee of Creditors (CoC) is formed to evaluate resolution plans submitted by prospective resolution applicants. If a plan is approved and sanctioned by the NCLT, the business is resolved, potentially with a change in ownership or management. If no viable resolution plan is approved within the stipulated timeframe (currently 330 days including extensions), the company goes into liquidation.

The Pre-packaged Insolvency Resolution Process (PIRP) for MSMEs:

Recognizing the unique nature and challenges of MSMEs, the IBC introduced the Pre-packaged Insolvency Resolution Process (PIRP) as a more efficient and less disruptive alternative to CIRP. PIRP is specifically designed for MSMEs and can be initiated by the MSME debtor itself, with the approval of its financial creditors.

Under PIRP, the existing management of the MSME largely remains in control (debtor-in-possession model), unlike in CIRP. The process is intended to be faster, with a maximum timeline of 120 days. The MSME proposes a base resolution plan to its financial creditors before initiating PIRP. If eligible and approved, the process aims to quickly evaluate this base plan or invite competing plans to reach a resolution.

Section 29A Exemption for MSMEs:

Another significant provision in the IBC beneficial to MSMEs is the partial exemption under Section 29A. This section generally disqualifies certain persons (like erstwhile promoters of an NPA account) from submitting a resolution plan. However, for MSMEs, this disqualification is relaxed under Section 240A, allowing erstwhile promoters, in many cases, to submit a resolution plan. This recognizes that for many MSMEs, the promoters are often best positioned to understand and potentially revive the business.

When to Consider Bankruptcy (IBC):

Initiating proceedings under the IBC, whether CIRP or PIRP, is a serious step and is typically considered when:

- The financial distress is severe, and the business is unable to meet its debt obligations even with MSME loan restructuring.

- The business model requires a significant overhaul or fresh capital infusion that cannot be achieved through conventional means.

- Creditor disputes are complex and cannot be resolved outside a formal legal framework.

- The promoters believe that the structured process under IBC, particularly PIRP, offers the best chance for a legally binding resolution or an orderly winding down of the business.

- Liquidation appears inevitable, and a process under the IBC can ensure a more equitable distribution of assets among creditors.

The Severity of Bankruptcy:

It is crucial to understand that initiating IBC proceedings signals significant financial failure. While PIRP is designed to be less disruptive, the process is still formal and has serious implications for the MSME’s operations, reputation, and the promoters. Liquidation, if resolution fails, means the business ceases to exist.

Making the Right Decision: A Step-by-Step Approach

Navigating financial distress requires careful consideration and informed decisions. Choosing between MSME loan restructuring, Lok Adalat, and bankruptcy depends on the severity of the situation, the underlying causes of distress, the viability of the business, and the willingness of stakeholders (especially lenders) to cooperate. Here’s a suggested approach:

- Comprehensive Financial Assessment: Get a clear picture of your MSME’s financial health. Analyze your cash flow, profitability, debt levels, and key financial ratios. Identify the root causes of the distress.

- Evaluate Business Viability: Honestly assess whether your core business model is still sound and capable of generating sufficient future cash flows to service debt. Can the business be revived with a new strategy or fresh investment?

- Explore MSME Loan Restructuring: If the business is fundamentally viable and the distress is temporary, approach your lenders proactively to discuss MSME loan restructuring. Prepare a strong proposal outlining your situation, revival plan, and proposed revised terms. Be ready to negotiate.

- Consider Lok Adalat for Specific Cases: If you have smaller loan accounts, particularly those classified as NPAs, explore the possibility of settling them through Lok Adalat. This can help clean up your balance sheet, even if it means a “settled” status on your credit report. Understand the potential settlement amount and your capacity to pay it.

- Assess the Suitability of IBC (PIRP): If restructuring is not an option or has failed, and the debt levels are significant, evaluate if a formal process under IBC, specifically PIRP for eligible MSMEs, is appropriate. Consider if there is a realistic chance of resolution or if an orderly liquidation is the necessary path.

- Seek Professional Guidance: This is perhaps the most critical step. Engage with experienced financial advisors, chartered accountants, and legal professionals specializing in MSME finance, debt restructuring, and insolvency. They can provide objective advice, help you analyze your options, prepare necessary documentation, and represent you in negotiations with lenders or during formal proceedings.

Conclusion:

Financial distress is a challenging phase for any MSME in India. However, it is not necessarily the end of the road. Understanding the mechanisms available, from proactive MSME loan restructuring and amicable settlements through Lok Adalat to formal resolution under the IBC, can empower MSME owners to make informed decisions. Early recognition of warning signs, transparent communication with lenders, a credible plan for the future, and seeking timely professional advice are crucial steps in navigating these storms. Whether through a revised MSME loan restructuring plan, a Lok Adalat settlement, or a formal IBC process, the goal is to find the best possible outcome for the business and its stakeholders, potentially paving the way for a renewed beginning.