Legal Notice Automation in Debt Recovery: The Missing Link Between Collections and Legal Action

When a borrower misses their third EMI payment, your collections team sends automated reminders via SMS, email, and WhatsApp. The borrower acknowledges the message, promises to pay “next week,” but doesn’t. After 90 days, the account becomes an NPA. Your legal team drafts a SARFAESI notice under Section 13(2), prints it, sends it via registered post, and waits. Three weeks later, you discover the notice was returned as “addressee not found.”

Meanwhile, your collections team has been calling the borrower daily. They have the updated address. They know the borrower relocated to Pune. But this information never reached the legal team because collections and legal operate in separate systems.

This is the fundamental problem legal notice automation is meant to solve. But most platforms in India today solve only half the problem.

The Two Worlds of Debt Recovery (And Why They Don’t Talk)

The Collections World

Collections teams live in a world of real-time data. They track borrower behavior across multiple touchpoints including payment gateway attempts, SMS delivery rates, WhatsApp message read receipts, call connection rates, and field agent visit logs. Their goal is simple: maximize contactability, increase payment intent, and close recoveries before legal escalation.

Tools they use: automated dialers, digital communication platforms.

The Legal World

Legal teams live in a world of compliance and timelines. They track SARFAESI notice dispatch dates, 60-day cure periods, DRT filing deadlines, court hearing dates, and advocate performance. Their goal is equally clear: ensure regulatory compliance, preserve legal rights, and enforce security interests when borrowers default.

Tools they use: case management systems, court tracking platforms, advocate networks.

The Problem

These two worlds rarely intersect. Collections teams escalate accounts to legal when they hit 90 or 120 DPD, hand over a static data file, and move on. Legal teams receive the file, draft notices based on outdated information, and proceed through a standardized workflow that doesn’t account for what collections learned about the borrower’s behavior, responsiveness, or payment intent in the previous 90 days.

The result? Legal notices sent to wrong addresses, borrowers who were responsive to digital communication never receiving legal follow-up, settlement opportunities missed because legal doesn’t know collections discovered the borrower recently sold an asset, and months of wasted time because the two teams operate in information silos.

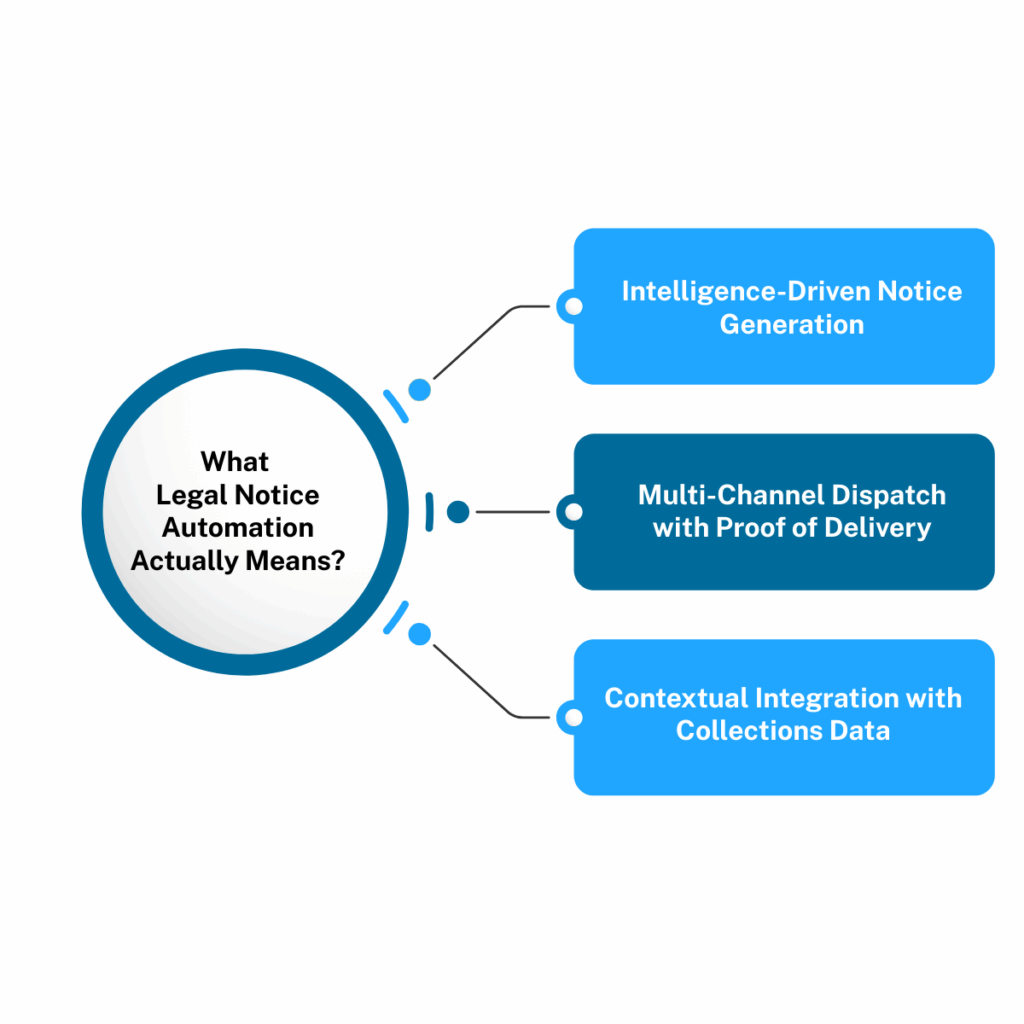

What Legal Notice Automation Actually Means (Beyond Just “Sending Notices Faster”)

When most people hear “legal notice automation,” they think of bulk email campaigns or automated post dispatch. But, real legal notice automation in debt recovery means three things.

1. Intelligence-Driven Notice Generation

Automated notice drafting based on loan type, default stage, security type, and jurisdiction. Legal notices aren’t one-size-fits-all. A SARFAESI notice for a housing loan with immovable property collateral looks different from a Section 138 notice for a personal loan with bounced cheque evidence. True automation means the system knows which template to use, auto-populates borrower details, loan specifics, and legal clauses, and generates notices that are legally compliant without manual drafting.

Example: Your legal team receives 200 new NPA accounts on Monday. Without automation, drafting 200 customized legal notices takes 3-4 days. With automation, all 200 notices are generated in 15 minutes, ready for review and dispatch.

2. Multi-Channel Dispatch with Proof of Delivery

Automated dispatch across digital channels (email, SMS, WhatsApp with PDF attachment) and physical channels (India Post registered post, courier with tracking). The critical piece isn’t just sending the notice—it’s tracking delivery. Did the email bounce? Was the SMS delivered? Did the borrower open the WhatsApp message? Was the registered post accepted or returned?

Example: You send a SARFAESI notice via registered post. India Post tracking shows “delivery attempted, addressee refused.” Your system immediately flags this for your legal team. They can now try alternate channels (digital delivery to known email/phone) or file for substituted service, rather than waiting 30 days to discover the notice was never received.

3. Contextual Integration with Collections Data

This is where most platforms fail. Legal notice automation that doesn’t connect to collections data is like GPS navigation without traffic updates—it gets you to the destination, but not necessarily via the optimal route. True automation means legal notices trigger based on collections behavior, not just calendar days. The system knows the borrower’s digital responsiveness, preferred communication channel, updated contact information from field visits, and recent payment attempts.

Example: Borrower has 120 DPD. Collections team notes that borrower responds to WhatsApp but ignores calls and SMS. Legal team sends SARFAESI notice. With contextual integration, the system automatically sends a courtesy WhatsApp message saying “Important legal notice dispatched via registered post to your address. Please contact us to discuss settlement options before enforcement action.” Without integration, legal just sends the registered post and waits.

The Legal Notice Journey in India’s Debt Recovery Landscape

Stage 1: Pre-Legal Reminders (0-90 DPD)

At this stage, communications are managed by collections teams. Automated reminders are sent via SMS, email, IVR, and WhatsApp. The messaging is soft, reminding, nudging, offering payment plans. This is NOT legal notice territory yet.

Stage 2: Demand Notice / Pre-Legal Notice (90-120 DPD)

The account is now classified as NPA. Before initiating formal legal action, lenders send a “demand notice” or “pre-legal notice” giving borrowers one final opportunity to settle. This notice is often sent by legal teams but still maintains a negotiation tone.

Key automation requirement: The notice must reference specific loan details, outstanding amount with interest calculation, and clear deadline. It should be tracked for delivery.

Stage 3: Formal Legal Notices (Post-120 DPD)

This is where legal action formally begins. Depending on the loan type and security, lenders issue Section 13(2) notices under SARFAESI Act for secured loans with 60-day cure period, Section 138 notices under Negotiable Instruments Act for dishonored cheques with 15-day payment demand, notices under Section 25 of Payment of Wages Act for employee loans, or arbitration notices if loan agreement contains arbitration clause.

Critical automation needs:

- Regulatory compliance: SARFAESI notices must follow exact format under Act

- Timeline tracking: 60-day cure period for SARFAESI, 15-day period for Section 138

- Proof of delivery: Essential for subsequent legal proceedings

- Multi-channel dispatch: Digital for speed, physical for legal validity

Stage 4: Post-Notice Follow-Up (Cure Period Management)

After sending legal notice, lenders must track whether borrower has responded within cure period, update case status if borrower initiates settlement, escalate to next legal step (DRT filing, asset possession) if cure period lapses without response, and coordinate between legal and collections if borrower engages.

Automation gap in most platforms: This is where collections and legal must work together. A borrower might call the collections helpline to negotiate settlement after receiving SARFAESI notice, but if collections can’t see legal notice status or legal can’t see collections notes, coordination breaks down.

Legodesk: The Only Platform Built for the Collections-Legal Intersection

What makes Legodesk different: Legodesk is the only platform in India that was purpose-built to bridge collections and legal operations for debt recovery. This means legal notices trigger based on collections behavior, not just calendar rules. Notices reference borrower’s digital responsiveness, field visit outcomes, and payment attempt history. Collections teams see legal notice status and timelines in real-time. Legal teams see collections notes, borrower contact logs, and settlement discussions.

Unique capabilities:

- Loan Intelligent (Conversational AI): Ask questions like “Show me all borrowers who received SARFAESI notice 30 days ago but collections team hasn’t followed up” or “Which borrowers responded to digital notice but haven’t responded to legal notice?”

- Contextual automation: Legal workflows that adapt based on collections data

- Unified workspace: One platform for both collections and legal teams

Ideal for: Banks, NBFCs, and ARCs managing secured loan portfolios where legal recovery is inevitable and coordination between collections and legal is critical for efficiency.

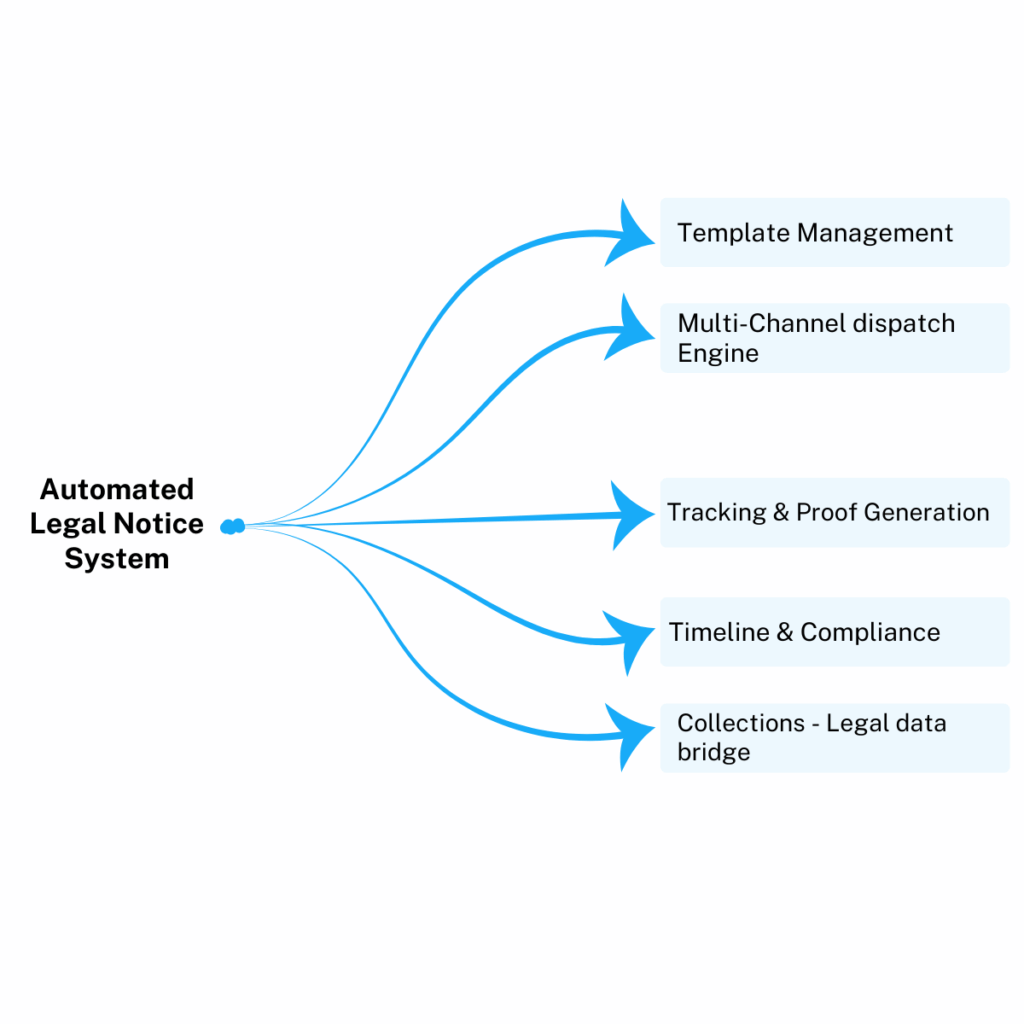

The Architecture of Effective Legal Notice Automation

Layer 1: Template Management

Pre-built templates for SARFAESI Section 13(2), Section 13(4), Section 138 NI Act, demand notices, and final settlement offers. Templates must be jurisdiction-aware (different state rules) and dynamically populate borrower data, loan specifics, interest calculations, and legal clauses from loan management system.

Layer 2: Multi-Channel Dispatch Engine

Digital delivery via email, SMS, WhatsApp, borrower app notifications. Physical delivery via India Post registered post, courier services, legal process servers. The system must support fallback logic, if email bounces, try SMS; if registered post is returned, trigger courier dispatch.

Layer 3: Delivery Tracking and Proof Generation

Real-time tracking of delivery status across all channels. Email opens and PDF downloads, SMS delivery reports, WhatsApp message delivered/read receipts, India Post tracking via API integration, and courier AWB tracking. Automated generation of proof of service documents for court submissions.

Layer 4: Timeline and Compliance Management

Automated calculation of cure periods (60 days for SARFAESI, 15 days for Section 138). Alerts before timeline expiry with flagging of cases where borrower hasn’t responded within cure period. Automated escalation triggers to next legal step if cure period lapses.

Layer 5: Collections-Legal Data Bridge

Real-time sync of borrower contact updates from collections to legal. Visibility of legal notice status in collections dashboard. Unified case notes accessible to both teams. Settlement workflow that updates both collections and legal status.

ROI of Legal Notice Automation: Beyond Time Savings

Time Efficiency Gains

Manual drafting: 15-20 minutes per notice. Automated drafting: 30 seconds per notice. For a mid-sized NBFC sending 500 legal notices per month, automation saves approximately 125 hours of legal team time monthly.

Cost Reduction

Physical notice dispatch costs: ₹150-200 per notice (print + registered post). Digital notice costs: ₹2-5 per notice. For lenders with high-volume portfolios, digital-first notice strategy with physical backup can reduce notice dispatch costs by 60-70%.

Recovery Rate Improvement

Faster notice dispatch means faster borrower engagement. Lenders using automated legal notices see 15-20% higher borrower response rates within cure period compared to manual processes, primarily because notices reach borrowers faster and through preferred channels.

Compliance and Audit Readiness

Automated proof of delivery eliminates documentation gaps for legal proceedings. Complete audit trail of notice dispatch, delivery attempts, and borrower responses. Reduces risk of cases being dismissed due to improper service of notice.

Implementation Checklist: What to Look for in a Legal Notice Automation Platform

For Collections Heads:

- Can the platform trigger legal notices based on collections behavior, not just DPD?

- Do I have visibility into legal notice status without switching systems?

- Can I see which borrowers responded to legal notices so I can prioritize settlement outreach?

For Legal Heads:

- Does the platform support all legal notice types we use (SARFAESI, Section 138, Arbitration)?

- Can I track India Post delivery status in real-time?

- Does the system automatically flag timeline violations (missed cure periods, approaching deadlines)?

For Recovery Heads:

- Does the platform connect collections data with legal workflows?

- Can I analyze which notice channels (digital vs. physical) drive higher borrower response?

- Does the platform support settlement workflows that update both collections and legal status?

The Future: From Legal Notice Automation to Legal-Collections Intelligence

Legal notice automation is just the beginning. The next evolution is conversational intelligence that synthesizes collections and legal data to answer strategic questions.

Instead of asking “How many SARFAESI notices did we send last month?”, lenders will ask “Among borrowers who received SARFAESI notices in the last 90 days, which ones showed high payment intent in collections phase but haven’t responded to legal notice, and should therefore get a settlement offer before we proceed to auction?”

This requires platforms that don’t just automate legal notices, but integrate collections behavior, legal workflows, and institutional knowledge to drive smarter recovery decisions.

At Legodesk, we’ve built exactly that. Our Loan Intelligent conversational AI sits on top of your unified collections and legal data, enabling recovery teams to make these complex decisions in seconds, not days.

Interested in seeing how legal notice automation works when collections and legal operate on one platform? Contact us for a demonstration.