Introduction

Goods and Services Tax (GST) is an Indirect Tax in India. It is levied on the goods and services at every step of the production process. However, it is refundable to everyone other than Final Consumer. The Tax came into effect on July 1, 2017, through the 101st amendment of the Indian Constitution. The Tax replaced existing multiple cascading taxes levied by the Government. Which means GST replaced many indirect taxes with a unified tax.

GST Migration

Migration is the process of issuing GSTIN (Goods and Services Tax Identification Number) to existing taxpayers. Here, the existing taxpayers are those who were registered under Central Excise and/or Service Tax before the commencement of GST. All existing registered taxpayers will receive provisional credentials in the ACES Portal. These credentials will help in log in to www.gst.gov.in. After verification of the mobile number and E-mail address, taxpayers have to submit the enrollment form. After verification of the enrollment form, GSTIN will be provided. To get registered with PAN http://www.incometaxindia.gov.in/Pages/tax-services/apply-for-pan.aspx

Read Also – Succession Right to Married Daughter in the Leased Premises

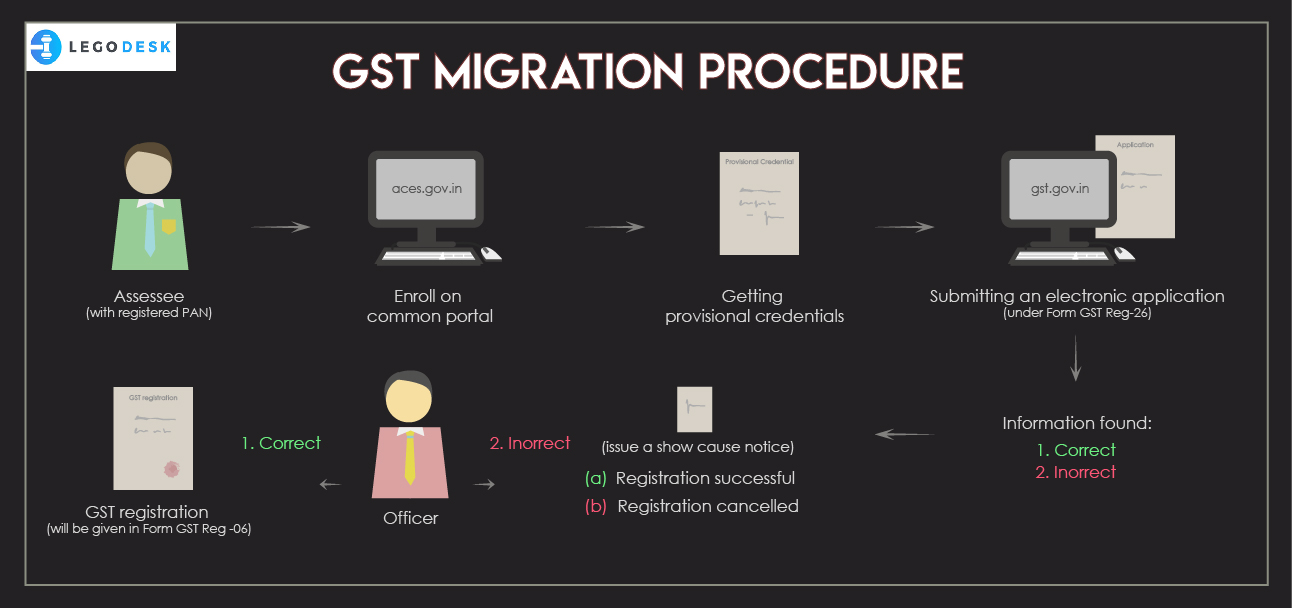

GST Migration Procedure

Before registration, the only requirement is that the Assessee must have a valid PAN (personal account number). Migration to GST is not allowable without PAN. Which means, an Assessee registered without valid PAN, needs to obtain PAN before migration to GST. Hence, the PAN number ssessee registered without valid PAN needs to obtain PAN before migration to GST. is important to get GSTIN.

-

Provisional registration

Obtaining Provisional credentials is the first and foremost step in the migration to GST. As per the Section-139(1) of CGST act, every Assessee needs to enroll on the common portal by validating the email and mobile number. This can be done through a facilitation center or directly logging into ACES https://www.aces.gov.in/. This is to ensure data privacy and security. Hence, log in to ACES is to ensure data your credentials are available with CBEC (central board of excise and custom).

To update email and mobile number as Central Excise (CE) Assessee – Click Here.

To update email and mobile number as Service Tax (ST) Assessee- Click Here.

Read Also – Filing a Patent Application in the United States

-

Final Registration

After getting provisional credentials, Assesse can log in to GST. Where he needs to submit an electronic application under Form GST Reg-26. Any information has to be submitted within three months. However, if the information is incorrect, the officer will issue a show-cause notice. A reasonable opportunity will be given to being heard. After that, unless if the reply to show cause notice is satisfactory, registration will be canceled. Whereas, if the information is correct, the final GST registration will be given in Form GST Reg -06.

Time Limit: Section 25(1) provides a 30 days limit for the registration. A person liable for registration should register himself within 30 days, from the day he becomes liable.

Different Scenarios for Existing CE Assesse:

-

Scenario-1

If the assessee has business premises and head office in the same State. The state code and PAN have to be sent to GSTN (Goods and Service Tax Network ). And, only one provisional ID will be provided. Moreover, if the Assessee has registration as a VAT dealer in the same State. No separate ID will be provided. Hence, under GST assessee can include more premises under CE registration as an additional place of business.

-

Scenario-2

If the assessee has registered business and head office in the different State – two separate IDs will be provided. Therefore, one for the head office and another for where business premises are located. Assesse can use them to log in to GSTN portal separately. And, they can get registered by filling up Form GST Reg- 20. However, if Assesse has registration as VAT dealer in the same state, the assessee may be issued none or one provisional ID.

Different Scenarios for existing ST assessee:

-

Scenario 3

If the assessee has one business premises in a State. They have to send State code and PAN GSTN (Goods and Service Tax Network ). And, only one provisional ID will be provided. Whereas, if Assesse has registration as CE and/or VAT dealer under the same PAN, the will not get a separate provisional ID. And, Assesse can include registered business and/or premises under ST registration as an additional business place.

-

Scenario 4

If the assessee has registration as Input Service Distributor. Also, he has one business premises in one place and many businesses address the different states where they distribute the tax credit. In such a case, they will not provide provisional ID to such assessee.

However, the Assessee would have to apply for fresh GSTIN through GSTN portal by filling up form 01.

-

Scenario 5

If the assessee has one registered office in one state. And, many different business premises in a different state from where they provide services. In such a case, different provisional IDs will be provided for each state with registered business and premises. Because they supply from all the premises which assessees own.

Whereas, the Assessee can use such IDs to log into the GSTN portal. Where he can complete the registration process by filling up form 20 to get GSTIN. However, The Assessee can include the registered premises as Principal or Additional place of business in the respective state.

However, in a case where Assessee, on the same PAN, has registration as VAT dealer. Here, they will not provide a separate provisional ID, as explained in Scenario 1.

Conclusion

The Goods and Services Tax is a unified and destination-based tax. It replaced all other existing indirect tax including Service tax and VAT. However, GST has many Advantages, while a few Disadvantages. Whereas the prices of some commodities have gone down, on the other hand, some products became costlier. The GST has directly affected businesses involved in buying and selling goods including services, in the Country.

Read Also – What are advantages and disadvantages of GST in India